2008 vs 2022 - Inflation Really is Different This Time

Core inflation is currently running at more than double its 2008 peak

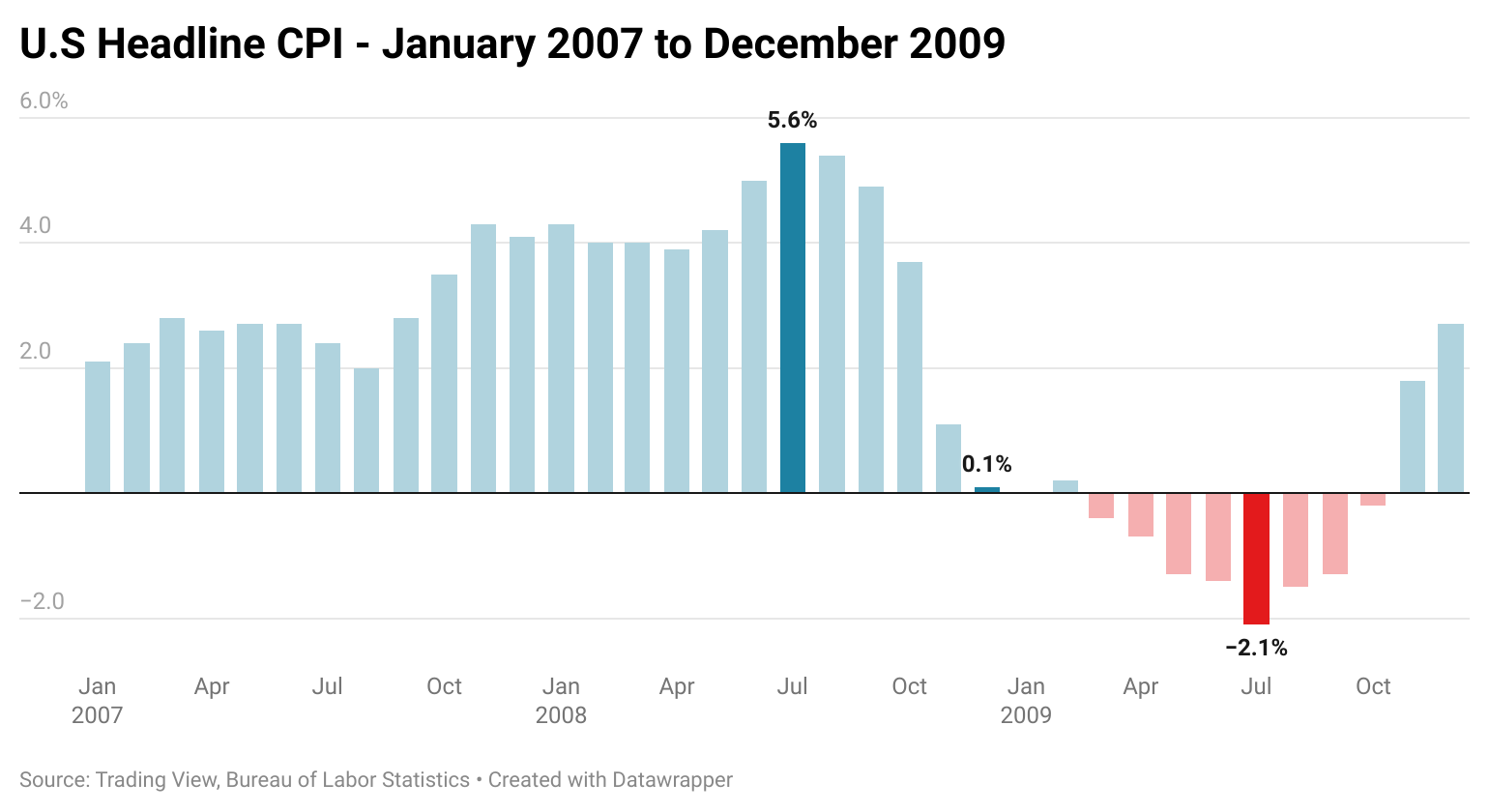

In 2008, the onset of the worst of the global financial crisis following the collapse of investment bank Lehman Brothers swiftly brought headline U.S inflation to an end. Between July and December 2008, headline inflation fell from its peak of 5.6% to just 0.1%.

With markets expecting the Fed to cut rates as early as Q2 next year, there is seemingly the perception that somehow inflation is going to be swiftly brought under control as it was in 2008, except this time without the largest financial meltdown since the Great Depression.

Now whether that is realistic or not, I’ll leave that to you the reader and the history books.

But when you examine the data, there are some major differences in the underlying inflationary pressures in 2022, when contrasted with 2008. Despite the relatively widespread perception that current U.S inflation is overwhelmingly driven by food and energy prices, that is not correct.

Ironically, it is correct when talking about inflation during 2008. At its peak, core U.S inflation (which strips out volatile items like food and energy) was just 2.5%, with headline inflation (which does include food and energy) running at more than double that at 5.6% due to swiftly rising energy and food prices.

Back in the present, core U.S inflation is running at 5.9%, its highest level since October 1982. While core inflation saw a recent run up to 6.5% in March, 5 out of its last 7 prints have been between 5.9% and 6.2%.

According to the Cleveland Fed’s monthly inflation Nowcast (based on a predictive model and various data inputs), core CPI is expected to rise by 0.48% month on month and 6.25% year on year in August.

Despite a great deal of commentary from across the spectrum of finance analysts and economic commentators that inflation has peaked, once you look at the core underlying inflation its clear that this kind of inflation could be far more persistent.

And therein lies the issue.

In December 2007, the United States entered recession as defined by the National Bureau of Economic Research (NBER). But the final peak in core inflation for this cycle didn’t occur until September 2008, the same month that Lehman Brothers collapsed and the Global Financial Crisis entered its most damaging phase.

Over the next 16 months core inflation would bounce around between 1.4% and 2.2%, before closing out 2009 still at a relatively robust 1.8%, just 0.7% below its peak.

Not even the worst financial and economic meltdown since the Great Depression was able to kill core U.S inflation quickly. It would be October 2010 before core inflation finally bottomed out at 0.6%.

This raises some rather uncomfortable questions back in the present. Core inflation remains strong and even if it were to begin a slow decline back toward the Fed’s headline inflation target of 2%, bar some sort of rerun of the GFC, it could take quite some time to get under control.

While falling food and energy would eventually provide some relief in terms of headline CPI if they follow the same script as every other U.S recession in recent decades. If core inflation continues to remain high, the Fed could have its hands tied in terms of loosening monetary policy.

With recession fighting U.S stimulus plans in the hundreds of billions now only found in the history books, the likely expectation that fiscal policymakers could deploy trillions in stimulus may give the Fed pause if they intend to continue their fight against inflation in this scenario.

Ultimately, the makeup of inflation in 2022 is drastically different to inflation back in 2008. Back then it truly was heavily driven by food and energy, while this time inflationary pressures are more broad based, with food and energy still playing a major role.

Some of the most dangerous words in the English language are “this time is different”, but based on the data we do have, that may actually be the case, as core inflation sits at heights not seen since the early years of Ronald Reagan’s presidency.

A major risk going forward is that Jerome Powell follows the same path as 1970s Fed chairman Arthur Burns, raising rates amidst high inflation only to loosen monetary policy before the job was finished, unleashing inflation for years to come.

This yo-yoing of inflation is arguably one of several central scenarios going forward. If the Fed gets cold feet in its fight against inflation amidst recession or is pressured politically into looser monetary policy, some degree of a rerun of the 1970s is arguably on the table.

Even under 2008 like conditions core inflation can take years to kill and with underlying inflationary pressures running at more than double GFC era levels, it could be years before fiscal and monetary stimulus can be deployed without a very real fear that inflation could come rocketing back.

— If you would like to help support my work by donating that would be much appreciated, you can do so via Paypal here or via Buy me a coffee. Regardless, thank you for your readership.

Thanks once again for your great insights.