Australian Investor Mortgage Demand Collapses

New investor loans down as much as 50%

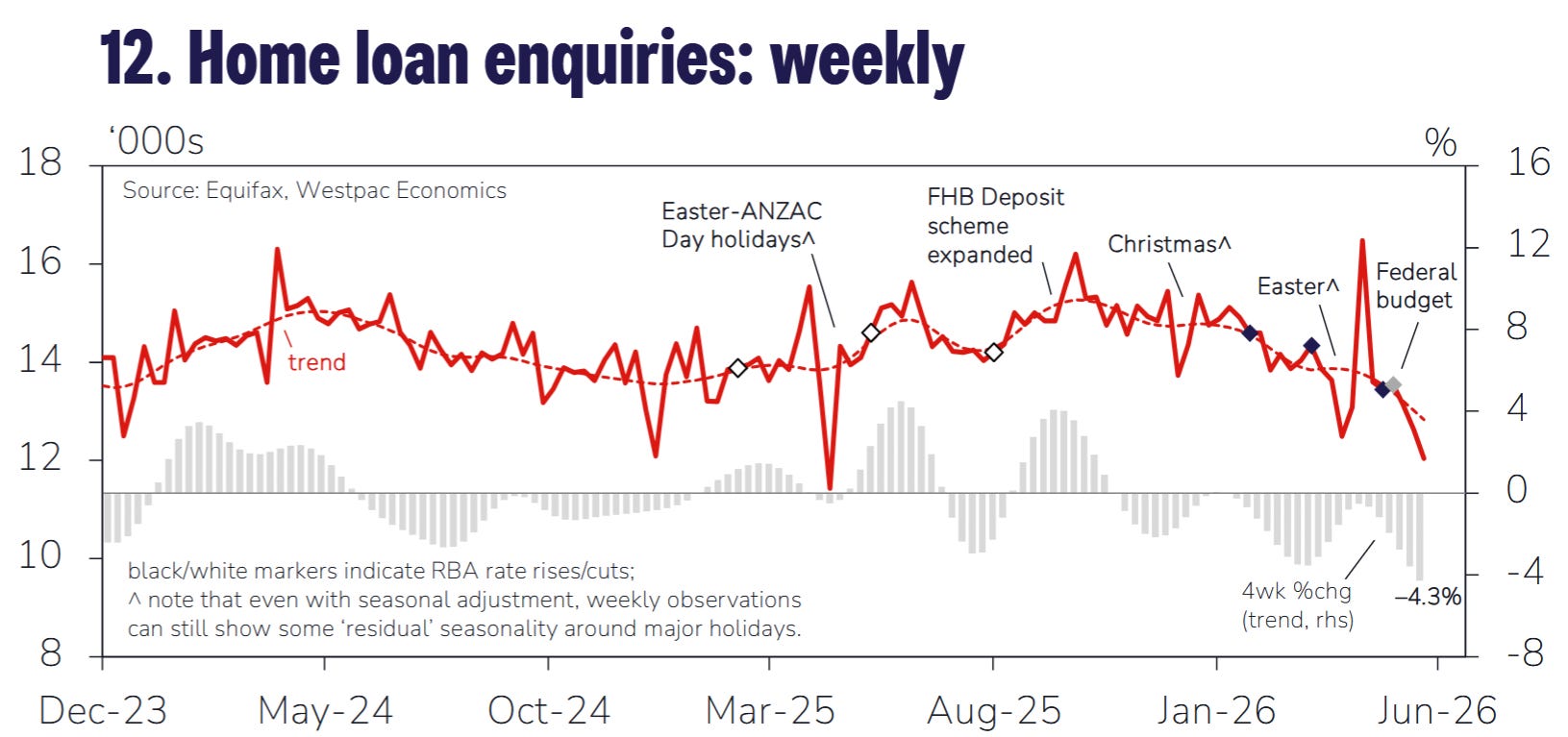

In the months prior to the recent federal budget, there was evidence in data from Westpac and Equifax to suggest that demand for new mortgages was trending down.

Given a backdrop of collapsed levels of consumer confidence stuck near all time record lows and falling levels of real consumer spending (ex-housing) in per capita terms, it’s perhaps unsurprising that demand for new loans had moderated in aggregate.

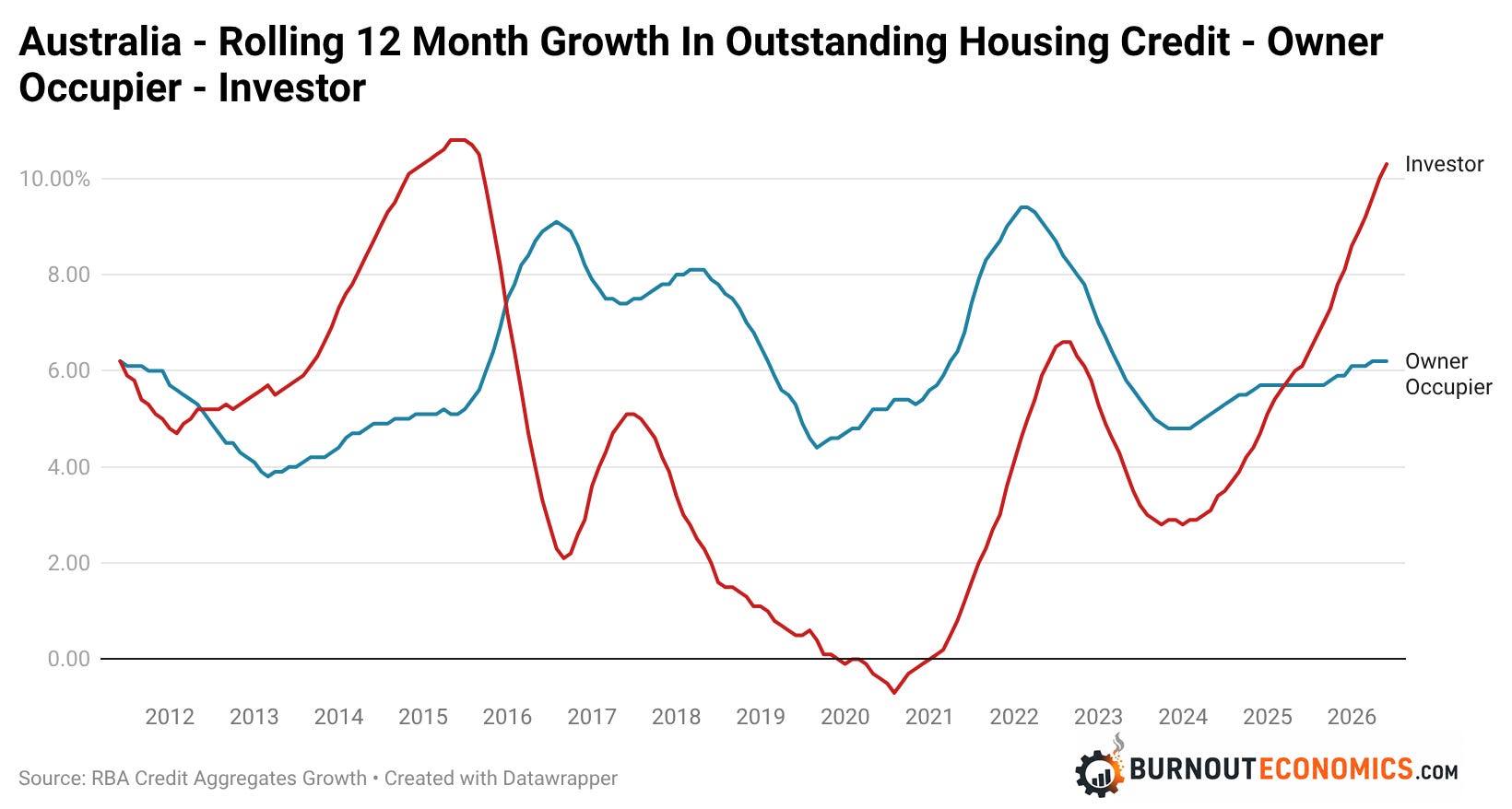

Looking at data from the RBA’s household credit aggregates, it’s clear that the relative moderation in the demand for mortgage credit in dollar terms did not stem from property investors, with total outstanding mortgage debt for property investors rising at the fastest rolling annual rate in more than a decade in May.

With the advent of the recent federal budget that has all begun to change dramatically.

According to recent commentary from senior Macquarie banks analyst Victor German to the Australian, demand for new investor loans is down as much as 50%, with overall new mortgage lending flows down 20% to 30% year on year.

Macquarie estimates that owner occupiers have not been immune to this shift, but the drop in this type of demand for new loans is far smaller, down 10% to 20%.

“This compares with Westpac’s application volumes tracking down 20 per cent year on year and NAB application values down about 15 per cent quarter on quarter.” German said.

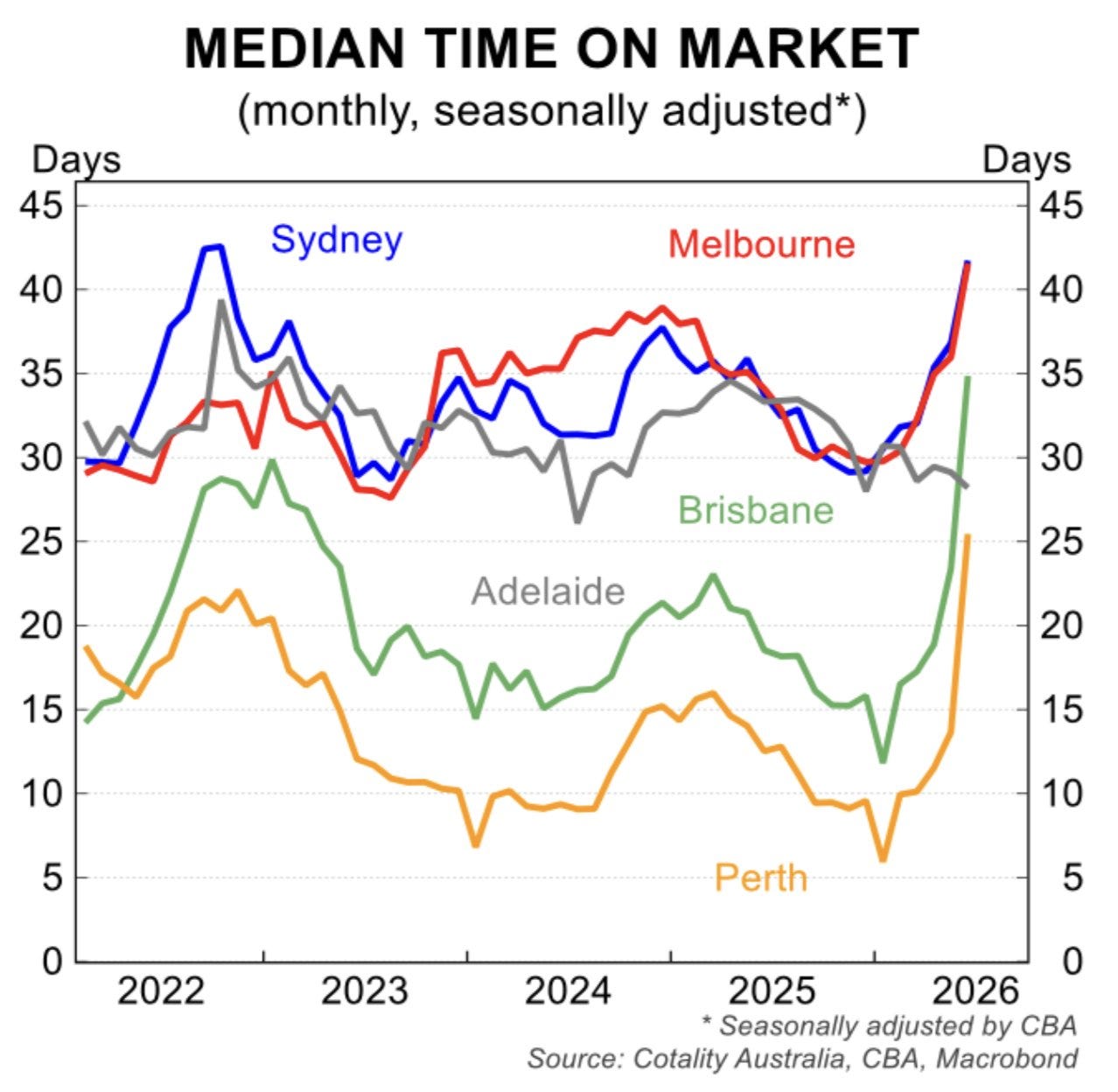

Amidst this dramatic reduction in demand for new mortgages, the amount of time homes remain for sale on the market has begun to surge, particularly in heavily under supplied markets such as Brisbane and Perth.

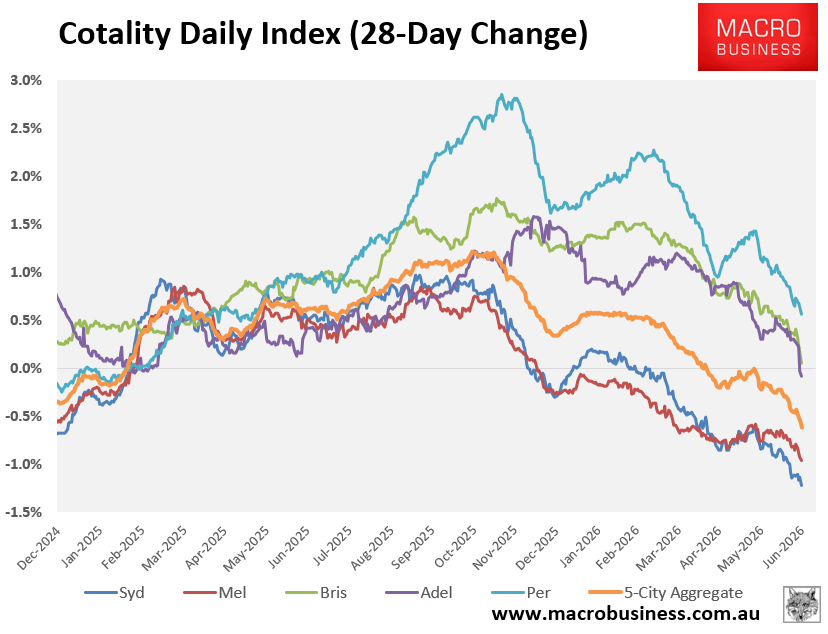

Meanwhile, amidst rising levels of stock and falling buyer confidence, price growth has moderated dramatically in the once hot minor capital city markets, while price falls have intensified in Sydney and Melbourne.

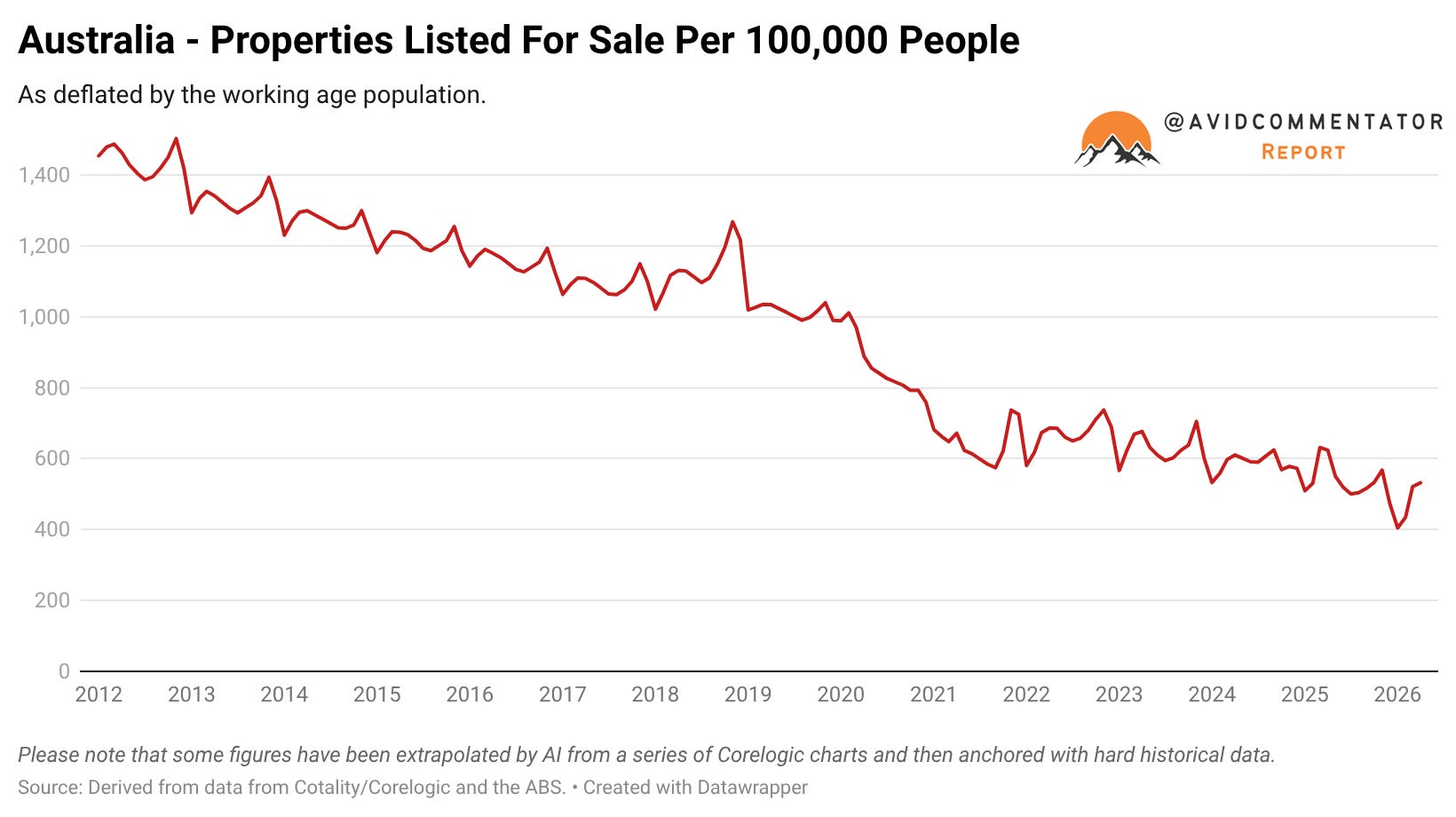

One of the major downside risks for the market on the road ahead is that overall stock on the market begins to trend toward normalizing to pre-Covid levels.

Based on listing data from Cotality, listing volumes in per capita terms (deflated by the working age population) are roughly half of what they were prior to the pandemic.

If stock on market was to move strongly toward pre-pandemic levels, the magnitude and likelihood of price falls would intensify dramatically in a vacuum.

In the words of SQM Managing Director Louis Christopher in his late June, auction clearance rate update:

“I think clearance rates are going to keep bumping along these levels for the time being, perhaps have some weeks which are a touch stronger. But then, in August we will get the seasonal rise in auction listings..and thats when things could get rather nasty for sellers.”

The Takeaway

The reality is that many of the elements that the support the valuations of the Australian housing market have been built on temporary factors and intervention from policymakers.

Low listing volumes were never going to persist forever, but the highly protracted nature of the depression in stock on market has played a major role in keeping prices high, as potential buyers battled over a far more limited pool of potential options.

Meanwhile, the pool of potential first home buyers who could be coaxed into the market through government interventions such as the 5% deposit scheme and shared equity programs is limited, with the pool able to pull the trigger on a purchase expected to dwindle dramatically over time.

Going forward there is the expectation that migration will stay high and that this will support rental price growth, as the rental crisis continues, thus helping to place something of a floor under housing prices.

The big risk for those hoping for stable or higher property prices on the road ahead is that this doesn’t happen. That some combination of political and/or economic pressure forces a cut to migration as it did in Britain, Canada and New Zealand.

Ultimately, if that scenario were to come pass without some other form of significant policymaker intervention to support the market, a housing crash scenario becomes far more likely.

— If you would like to help support my work by making a one off donation that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Thank you for your readership.