Australia's Boomer Powered Consumer Economy And What It Could Mean For Inflation

Hard data on the different spending and wage outcomes of Australia's different age demos

To say that Australia has a unique economy when compared with most of its developed world peers would be something of an understatement. According to the Harvard University Economic Complexity Index, the Australian economy is the 91st most complex out of the 133 nations compared. The most recent report revealed that one of Australia’s closest rival over the past few years on the index, Uganda, had improved its economic complexity to now sit four places above Australia.

A popular phrase for Australian economists is that the economy is built on houses and holes, aka construction, real estate, banking and the resources sector. But when it comes to the consumer economy there is another driver, actually one of remarkably few engines of growth within this sector still functioning, Baby Boomers.

The ‘Real’ Aussie Economy

Despite the reputation of the ‘Australian Economic Miracle’ which is derived from avoiding a recession for almost 30 years prior to the pandemic, the reality is quite a bit more challenging.

According to data from the federal governments productivity commission, for Australians under the age of 35, between 2008 and 2018 growth in their real wages went nowhere. Technically speaking there was actually a small contraction for some demographics in that age group.

Meanwhile, the real wages growth of older demographics performed relatively well, despite being somewhat below the longer term trend.

According to data from the RBA and ABS, real household consumption for households with a reference person aged 15-24 peaked in 2009, while peaking for those aged 25-34 in 2007.

Even among the 35-44 demographic, household consumption growth between 2007 and 2018 was relatively anaemic relative when contrasted with that of older demographics. With this demographic in particular holding a high level of debt and often lacking in the high levels of equity that underpins consumption for older Australians, its perhaps understandably why consumption growth has been so poor despite the growth seen in real wages in the decade to 2018.

When looking at older demographics, the older they get, the more their real household consumption has grown. Which brings us to a major driver of the Aussie economy and household consumption, home equity withdrawals.

Equity Mate….

In the late 1990s, Australia’s largest bank the Commonwealth Bank ran an TV advertising campaign which encouraged mortgage holders to withdraw cash from their mortgages to fund all manner of consumption from new cars to holidays. When the everyman mortgage holder in the original commercial asked how his neighbour managed to afford his new holiday home, he famously replied “Equity mate!”.

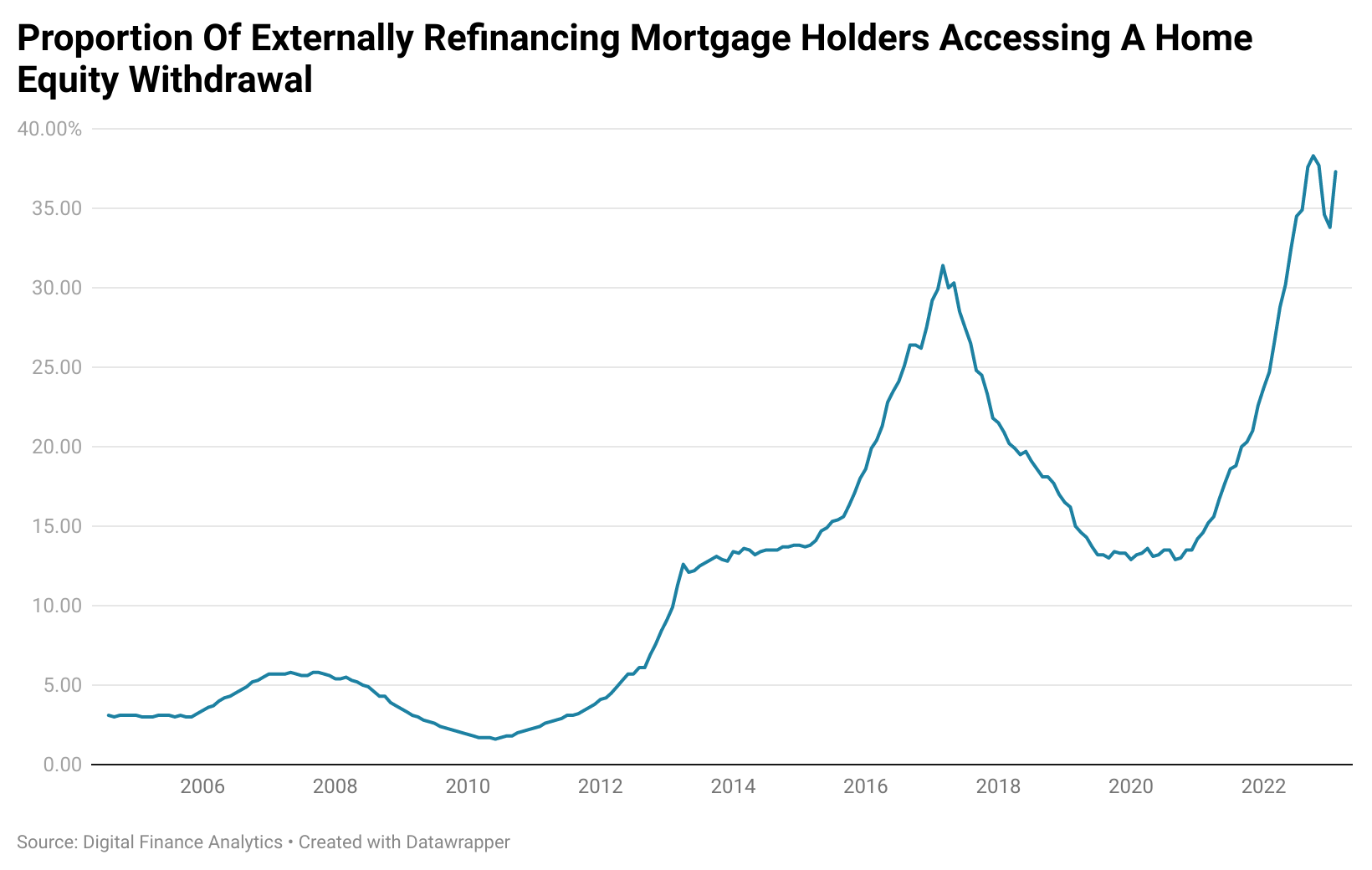

In the decades since home equity withdrawals have gone from a relatively fringe financial product, to representing over 1/3 of all mortgages holders externally refinancing (refinancing their loan with a different institution) and over 4.6% of GDP.

To put this into perspective, during the period Americans were being chastised for using their homes as ATM’s in the run up to the global financial crisis, home equity withdrawals as a percentage of GDP peaked at 2.65%.

When confronted with rising rates, Americans were also relatively prudent, reducing their home equity withdrawals by almost half prior to the U.S entry into recession in December 2007.

In Australia things are playing out quite a bit differently. The proportion of borrowers withdrawing home equity continued to rise in the face of higher interest rates. Unfortunately despite repeated requests of the relevant agencies we don’t have updated figures on the exact dollar value of recent home equity withdrawals.

While borrowing additional funds against a property, particularly one’s own home may seem foolhardy to some of you, in Australia its often just part of many households choose to live their lives. It can also make a manner of sense when looking at a case study.

For example, a Sydney based Baby Boomer couple in their early 60s bought their home in 1995 for $196,000. Since then their median house has moved to the 75th percentile, amidst an explosion in the size of the city, the number of dwellings and its population in the last 28 years.

Today that $196,000 home is worth almost $1.9 million, the household is almost debt free and has more than enough equity to fund whatever holiday, car or other purchase they can possibly think of, safe in the knowledge they are sitting on a war chest in home equity.

But more than that, they are often also psychologically insulated against any potential downside, because of the belief that “they” (RBA, APRA and various levels of government) won’t allow anything bad to happen to the housing market. Whether that assertion is true or not is rather irrelevant, as it continues to provide fertile ground for further home equity withdrawals even in the face of rising rates and a deteriorating economic outlook regardless.

Household Savings

When it comes to household savings balances, the 55-64 and 65+ age demographic amassed the largest amount of savings above trend during the pandemic. Putting away an additional $192 billion compared with the pre-Covid trend. As of the end of June 2022, Australians 55 and over held $926 billion in household savings.

In this Australia is not unique, households around the globe built up large levels of new savings during the pandemic. But what is interesting about Australia is that we have confirmation that the spending of older demographics continues to grow at a rate significantly faster than inflation, even as wages and broader income growth continues to significantly underperform headline inflation.

We’ll get into the most recent hard numbers on household spending by age demographics in just a moment.

The Boomer Powered Consumer Economy

As more and more of the traditional engines of the Australian consumer economy flame out, it has become even more reliant on the consumption of older generations and ensuring that the housing market that helps to underpin that consumption doesn’t take a big tumble.

Rather than the 18-49 or 25-54 demographic being the engine of household expenditure growth and the broader consumer economy as was the case historically, it is now older Australians who are overwhelmingly the driver of the consumption growth.

For those wondering why I chose the 18-49 and 25-54 demographics as comparison points, they are historically the prime target for advertisers due to their high levels of consumption.

In a recent analysis by Commonwealth Bank, it was found that spending per capita for all age demographics under 55 were falling relative to the rate of headline inflation. Meanwhile the average spending growth of demographics over 55 was pushing 10%, significantly above the rate of headline inflation.

Boomers, Monetary Policy And Inflation

This raises some rather challenging questions for the RBA and other central banks faced with a high proportion of variable rate mortgages and a large wealthy older cohort.

The demographics that generally have large mortgages and are the most exposed to rate rises have already cut their consumption growth to significantly below the rate of inflation, while older generations continue to spend strongly, further stoking inflationary pressures.

Part of the issue is that during prior monetary policy tightening cycles in high inflation environments households would react accordingly and begin to batten down the hatches in anticipation of what laid ahead. In the present, the same generation that tightened their belt hard in the run up to the 1990s recession is now not only not negatively impacted by higher rates, but benefitting from them in the form of higher savings rates.

There is no real historical analog for this set of circumstances, where such a large affluent older demographic was not exposed to rising rates, while a majority of younger generations were exposed to higher mortgage rates or higher rents.

There is also I like to call the ‘YOLO Effect’. YOLO meaning “You only live once”.

Where once YOLO was the preserve of younger generations and a catch phrase before doing something potentially risky, it is now a part of the collective psyche of people more broadly following the pandemic.

After years stuck inside due to lockdowns and various Covid-19 driven restrictions, people of all ages are keen to get out there and live their best lives. The big difference being that older demographics have the incomes, savings and/or equity to pursue those goals, while younger generations tend to be more focused on keeping up with the cost of living out of sheer necessity.

With the YOLO effect well and truly in play, over $200 billion in excess savings in the old war chest and trillions of dollars in equity, older demographics could keep spending for years to come without encountering any major issues if all things were to remain equal, at least in aggregate.

After seeing the largest short term run up in asset prices and net wealth in history, this is not just an issue for the RBA and Australia, but for many developed world central banks.

Interest rates will likely eventually be effective in driving a U.S recession, but how much does the economy and asset prices need to deteriorate in order to dissuade continued strong household consumption from older more affluent households?

That question is a big one for central banks and a challenging answer to quantify.

But for Australia, the challenge is arguably even greater. There is no memory of a difficult recession relatively fresh in the minds of households, there is over $7 trillion worth of home equity and through the perceived support from policymakers a willingness to continue to use it to fund consumption.

Ultimately this economic cycle is different to those in the past, but while the end result may not repeat, there is a high likelihood that it will eventually rhyme.

— If you would like to help support my work by donating that would be much appreciated, you can do so via Paypal here or via Buy me a coffee. Regardless, thank you for your readership.

If you would like to support my work on an ongoing basis, you can do so here via Patreon or via Paypal here

What will be the implications of the boomers starting to die off?

top blog entry AC, as usual. Thank you