Australia's Failed Economic Strategy

Latest National Accounts Edition

Coming this weekend for paid subscribers (with something for everyone), an article on when housing prices will become affordable by city and at a national level.

And a big thank you to all of you have become paid subscribers or made a contribution, it is immensely appreciated.

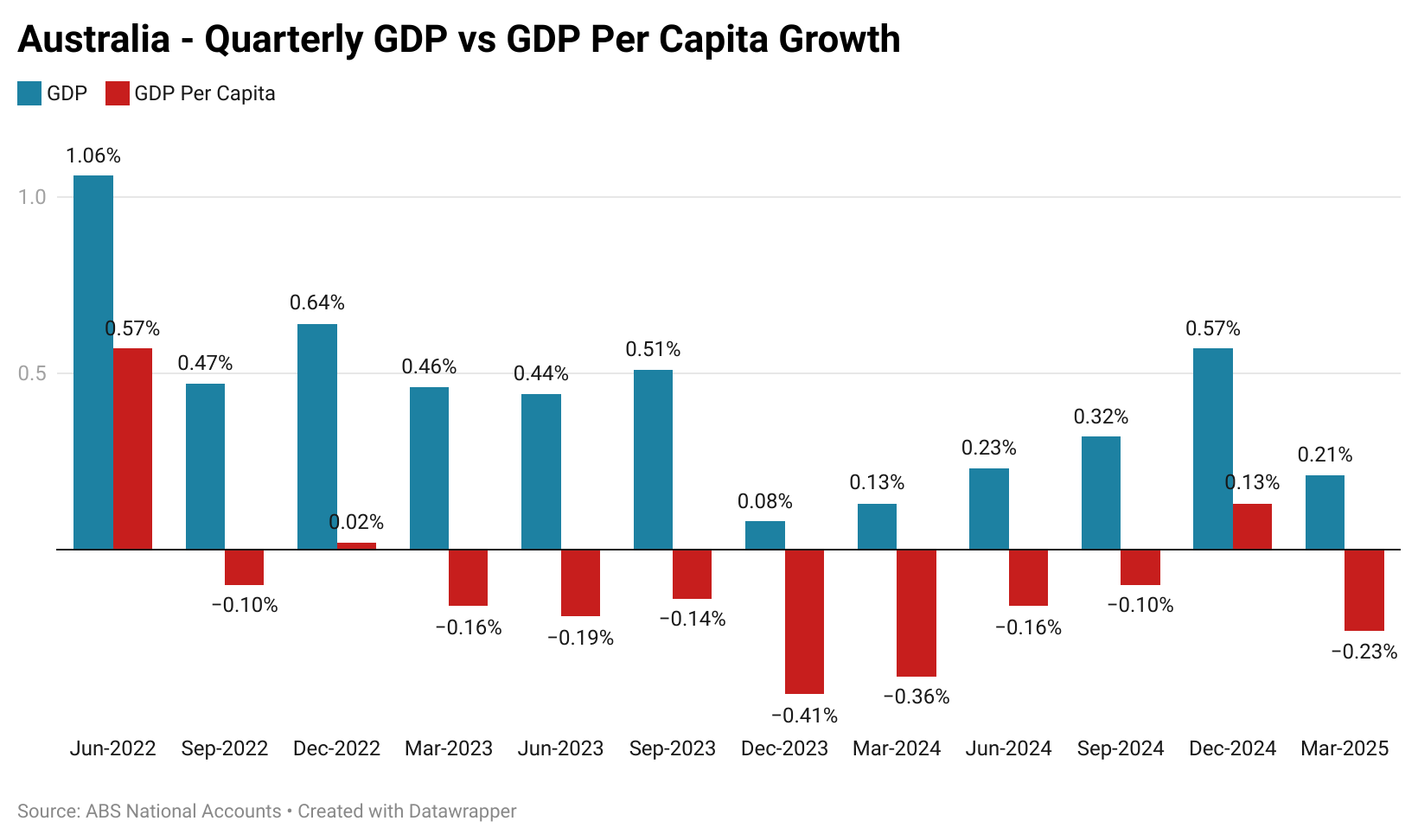

With the release of the latest national accounts data, it was revealed that Australia’s GDP in per capita terms is one again contracting. Meanwhile, in headline GDP terms the economy grew by 0.2%, surprising to the downside of the analyst consensus of growth of 0.4%.

Australian GDP per capita has now contracted in 9 of the last 11 quarters, its most concentrated series of falls since records began in 1973.

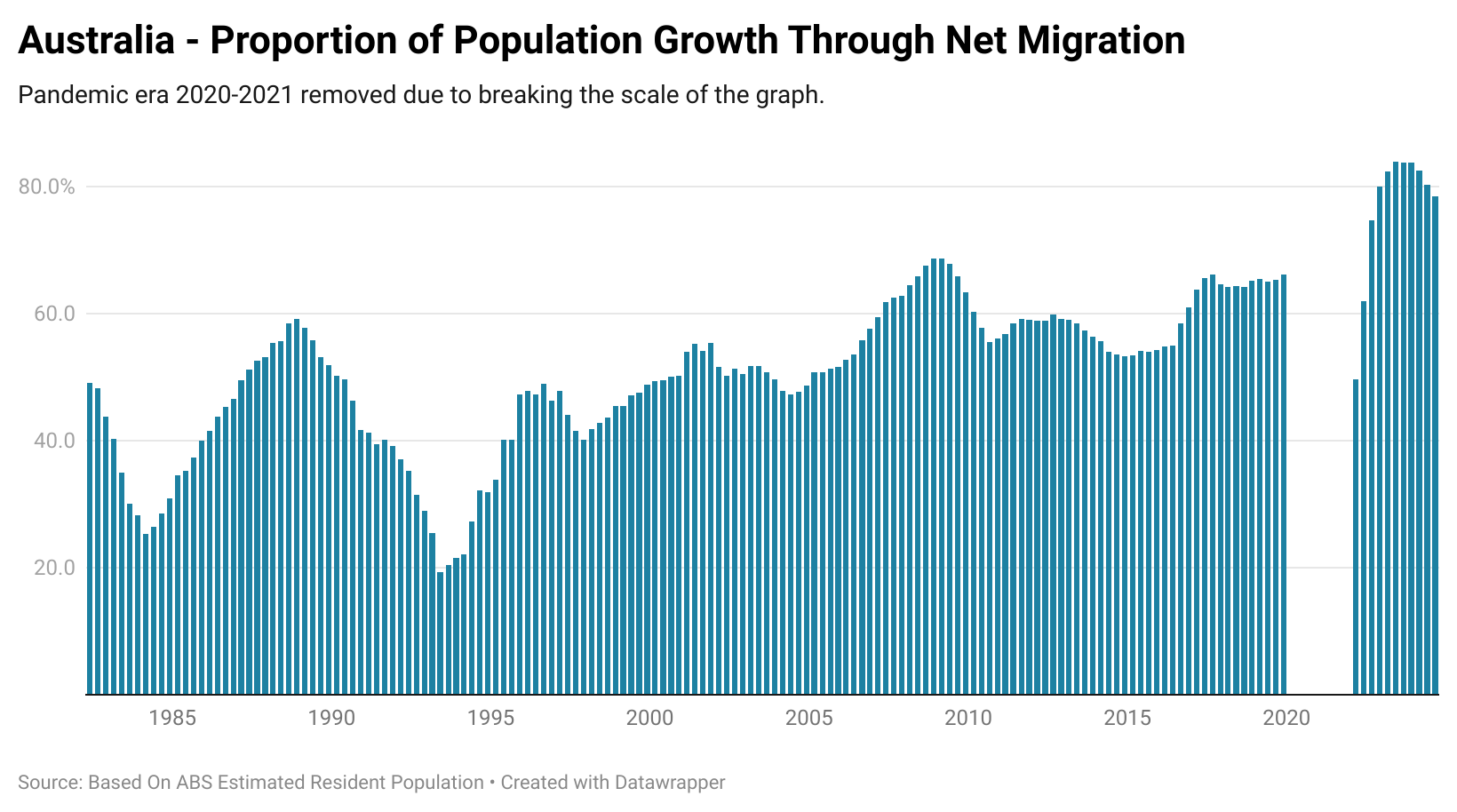

But this is actually masking an even more severe deterioration in the output of the economy. In decades passed, a far greater proportion of net population growth was driven by the natural increase, aka births minus deaths.

Today, the overwhelming majority of Australia’s population growth is being driven by working age migrants.

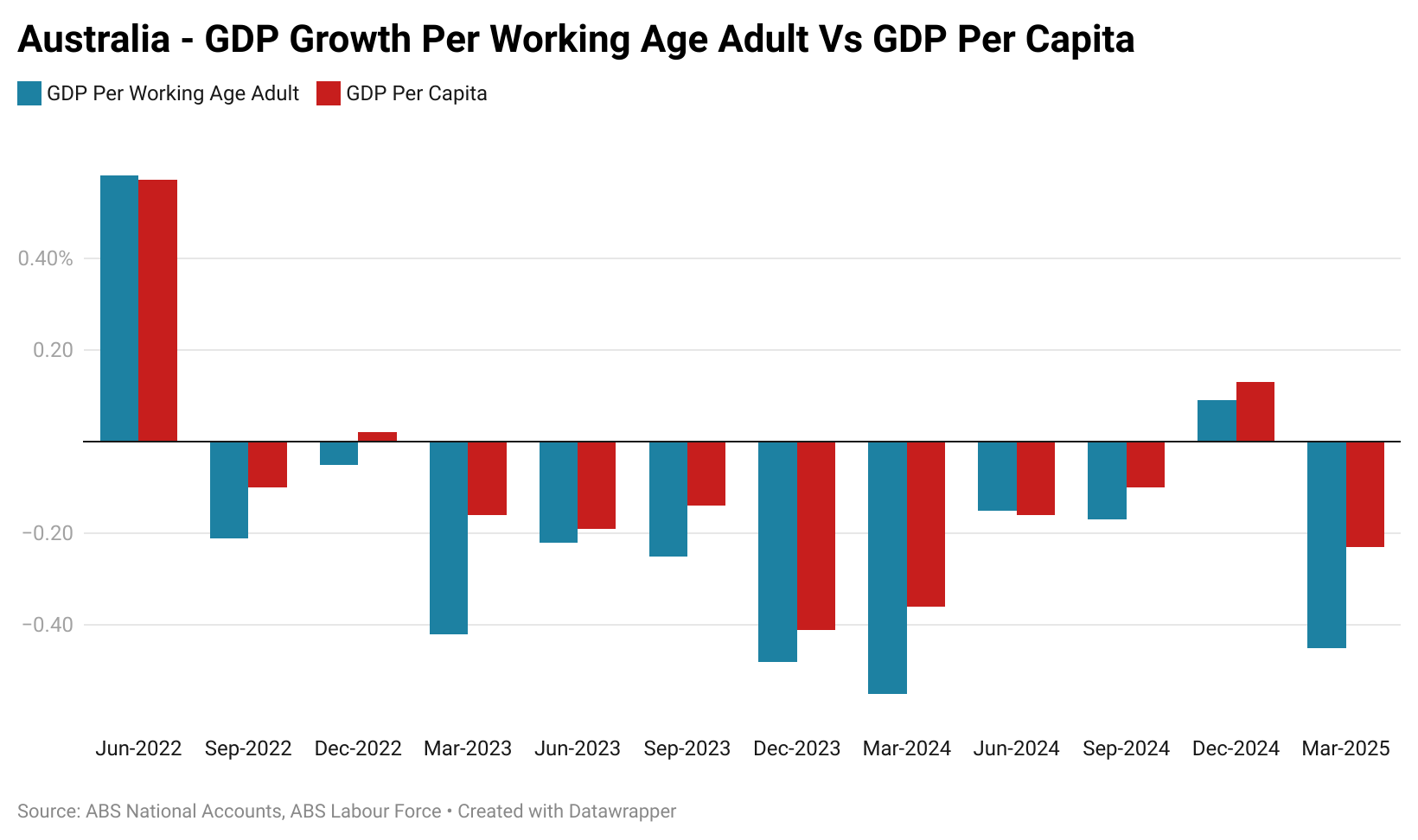

So if we shift our perspective from the traditional metric of GDP per capita, which divides economic activity across the entire population to one where it’s divided by only those of working age (aged 15 and over), an even more concerning picture emerges.

As illustrated by the chart below, the falls become significantly larger.

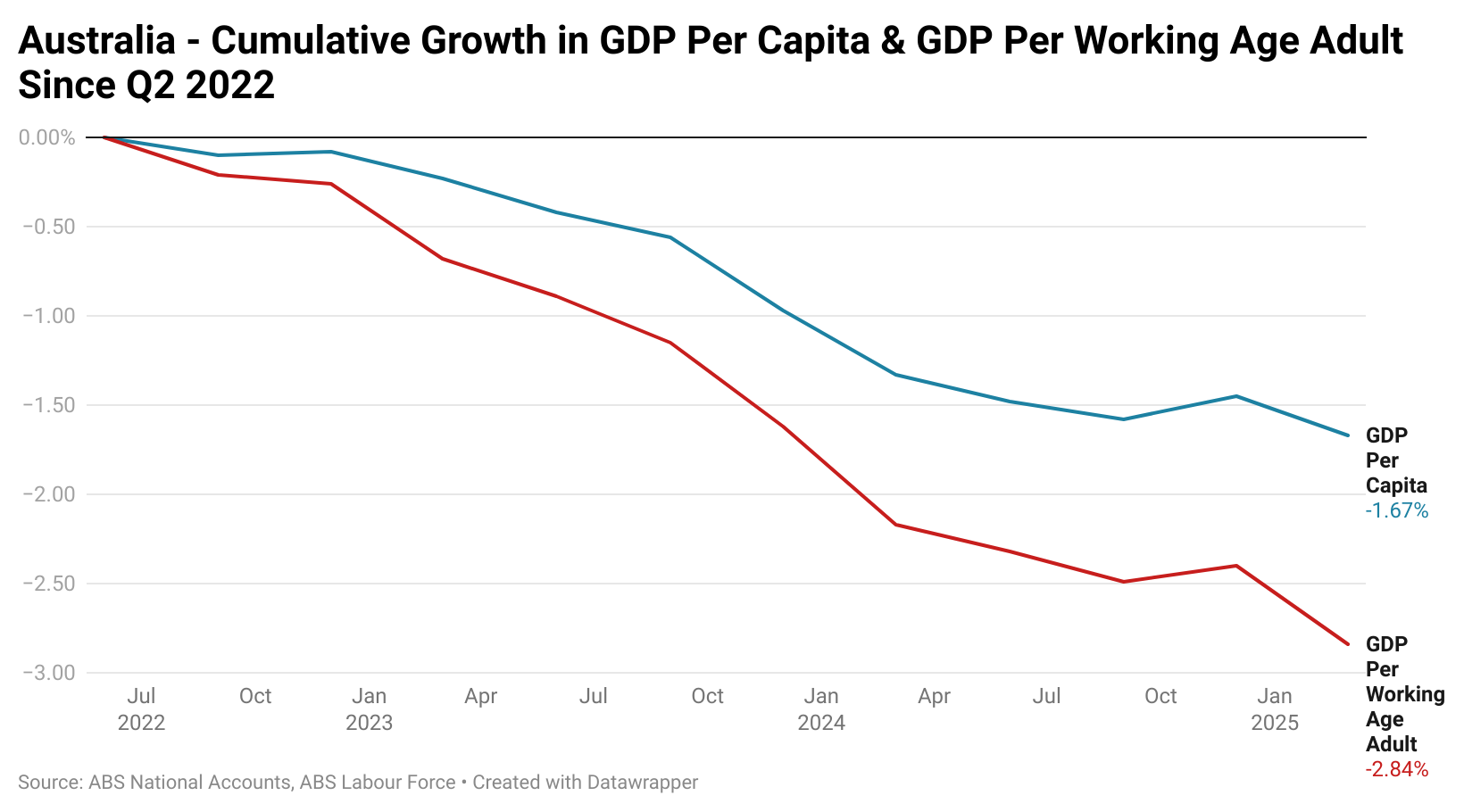

If we zoom out and look at growth in per capita and per working age population member cumulatively since the last strong growth in Q2 2022, it reveals an economy that looks rather poorly.

On this metric GDP per capita has contracted by a cumulative 1.67% since Q2 2022, with GDP per working age adult contracting by a significantly larger 2.84%.

While the consensus expectation is that interest rate cuts will spur a resurgence in the economy and boost GDP per capita at least somewhat, I’m more skeptical.

Since the start of the pandemic the overall level of household savings and the income derived from it has increased dramatically, to the point where interest on savings is now equal to over 7% of all employee earnings up from 2.9% in the first quarter of 2022.

In some ways Australia now faces a similar issue to China. As interest rates are cut mortgage holders have more cash to spend, but deposit holders have less. This shift is also intensified by the ongoing growth in spending by older demographics, so the income derived from savings is arguably on average more likely to be spent than it was a decade ago.

If we assume all currently priced in rate cuts are passed on in full to savers and mortgage holders (admittedly a huge if), the net effect annually is conservatively $3 billion a year. Naturally there is the issue of taxes on savings (if applicable) and the disposition of mortgage holders to spend, but ultimately it’s a figure that even overestimated is less than 0.2% of GDP.

Ultimately, the strategy of policymakers defined by high levels of migration and extreme levels of taxpayer funded job creation is not working for the Australian people and there is precious little sign the outcomes derived from the strategy will improve any time soon.

— If you would like to help support my work by making a one off donation that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Thank you for your readership.