Australia's Recession Prospects In 4 Charts

The largest rise in mortgage servicing costs ever and the worst real wage outcomes in over 30 years

In recent weeks, the prospect of an Australian recession has gone mainstream, with the Commonwealth Bank putting out a note suggesting that the economy falling into recession was roughly a 50/50 call. It was joined shortly after by HSBC, which also ascribed a 50% probability that the economy would enter a recession.

So I thought I would put together this short piece on the four charts I think are key to the fate of Australia’s domestic economy.

Mortgage Repayments Rocket

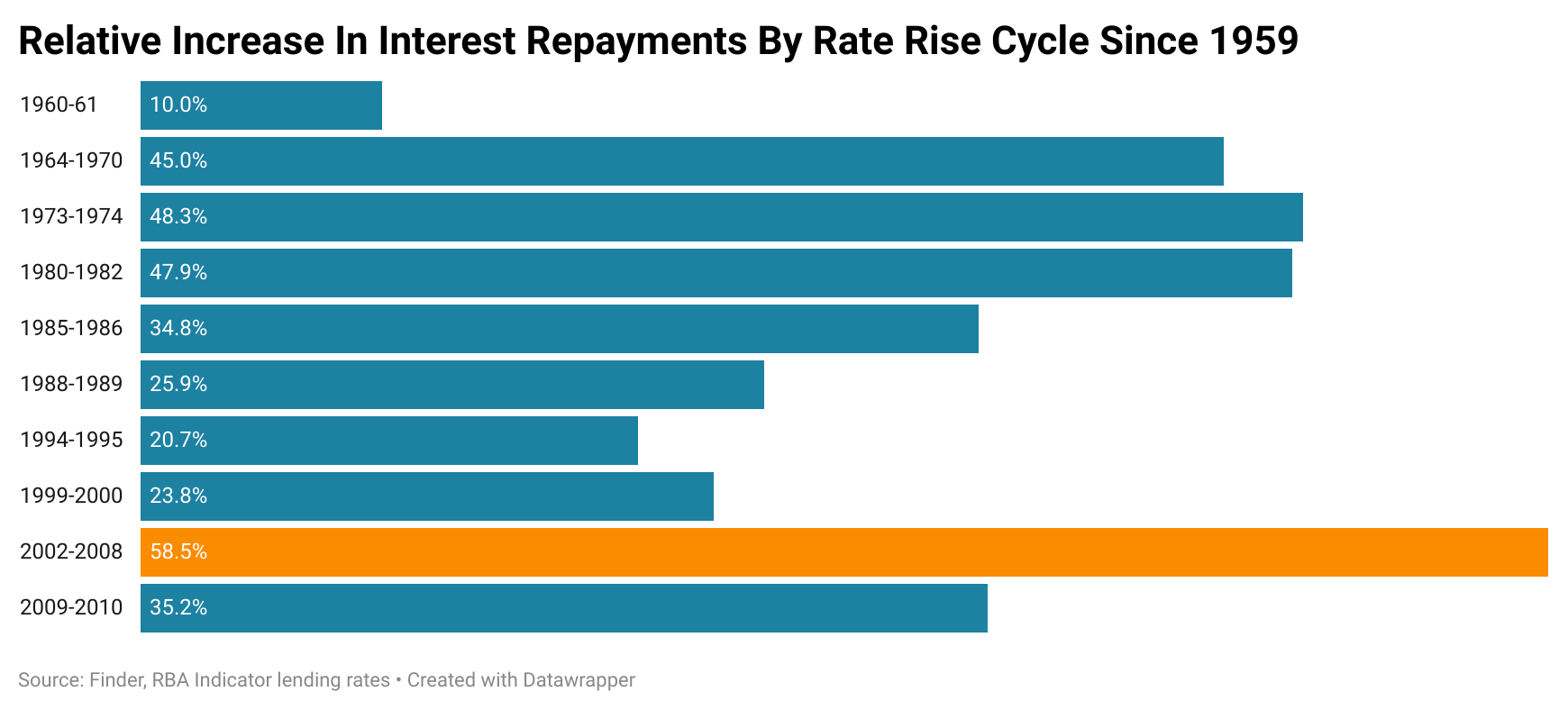

Back in May 2022, I wrote an article for News.com.au detailing the magnitude of the increase in mortgage repayments that occurred during historic rate rise cycles. Of the ten cycles that occurred between 1959 and 2010, the largest increase in mortgage interest repayments in a single cycle was 58.5%.

According to data from the RBA, the current rate rise cycle has seen mortgage interest repayments rise by 121.0% based on the average payable variable mortgage rate. This is more than double the previous record high increase and it also occurred over 13 months, instead of 6 years.

But this is actually significantly understating the true scale of the problem.

Throughout late 2020 and much of 2021, fixed rate loans were written at an average of just 2.04%. Fast forward to 2023, these loans are now in the midst of the largest wave of expiry’s in the overall fixed rate loan book.

Except unlike borrowers who have been on the variable rates the whole time who have seen their interesting repayments rise by 121.0%, these households will see their interest repayments rise by 209.8% based on reverting to the average payable variable rate today.

To say this is a challenge compared with past rate rise cycles would be an understatement. Its also worth noting that these numbers are based on today’s RBA cash rate and at least one more rate rise is now a consensus call, so the challenge could still become even greater.

Real Wages Growth

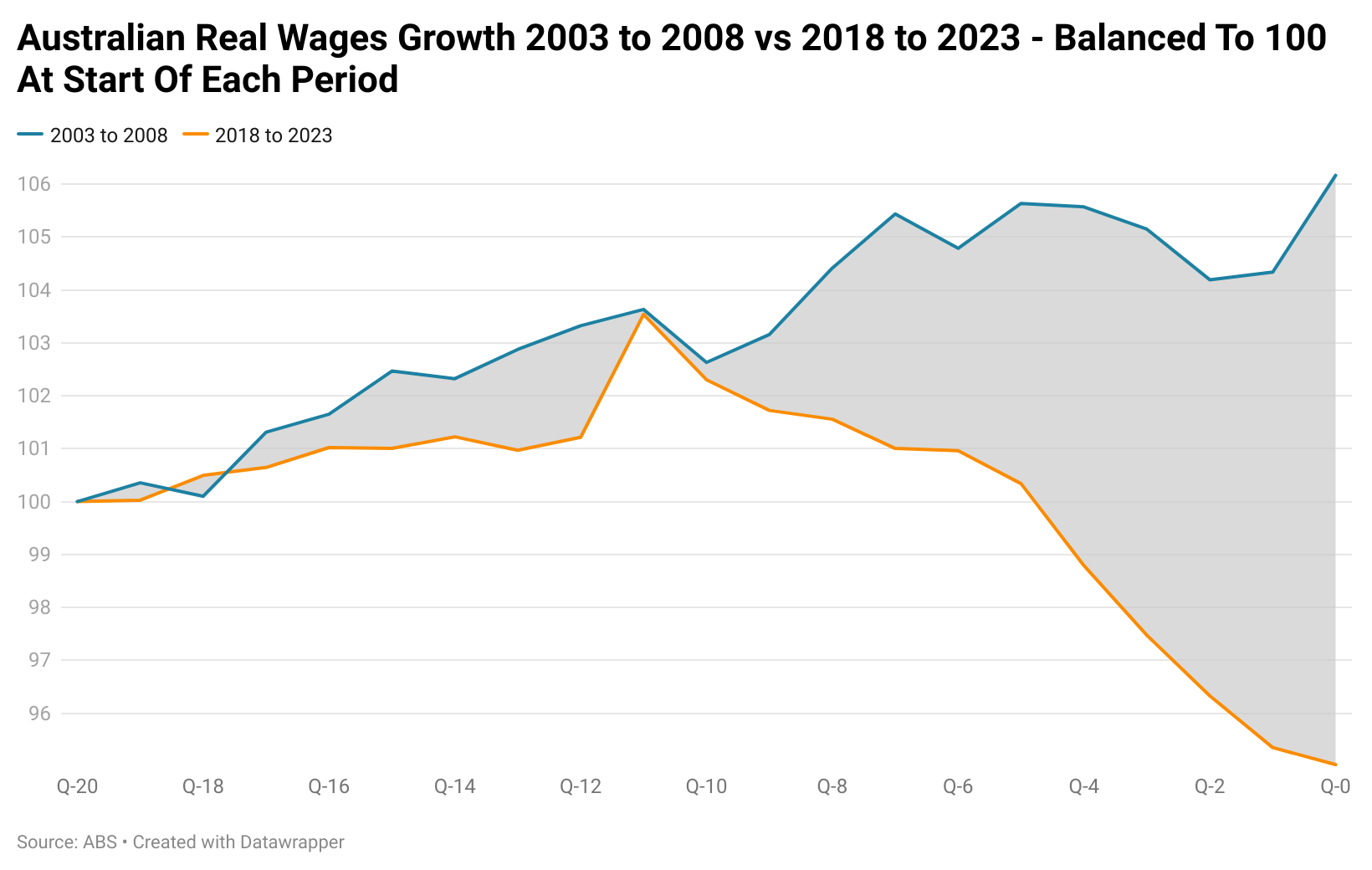

In the run up to the global financial crisis, years of strong real wages growth helped to insulate households against rising inflation, rising rates and the economic downturn that followed. In the 5 years prior to the GFC, inflation adjusted wages grew by 6.2%.

Back in the present, things aren’t nearly so rosy. Over the past 5 years real wages have declined by 5.0%. With inflation still running at a rate 3.3% higher than wages and forecasts that expect this state of affairs to continue until some time during 2024, the deterioration in household purchasing power is set to continue.

Dodging the global financial crisis recession took several major factors going Australia’s way and more than a little bit of luck. But this time the performance of real household purchasing power growth is not only not a tailwind at the economy’s back, it’s likely to drag significantly on the performance of the consumer economy at a highly inopportune time.

While aggregate spending is holding up somewhat as I detailed in a previous article, the reality is that the growth in spending is being done by those in demographics over the age of 55. As long as that holds up, the economic picture will be flattered by their consumption growth. But if that was to revert to some degree of the mean on the back of a market downturn or recession, then things could get quite a bit more challenging relatively swiftly.

Relative Increase In Repayment Burden

Back in March AMP Capital’s Chief Economist Shane Oliver produced this chart to illustrate that at a 4.1% RBA cash rate, mortgage repayments would reach a record high as a proportion of household disposable income.

That in and of itself is a rather concerning statistic, particularly given that all Australia’s big 4 banks have now pencilled in a cash rate that is going to head even higher in the coming months. But like with so many things in the world of finance and economics, one of the key factors is the rate of change.

For example, that little black circle on the graph below marks the rise in the RBA cash rate to 17% in the run up to Australia’s last pre-Covid recession.

Through a combination of high inflation, a 3.5% increase in interest rates from 13.5% to 17.0% and domestic economic issues, Australia experienced a highly challenging recession. In the years during and immediately following, the unemployment rose by 5.4% to 11.2%, the highest level since the great depression.

Its at this point that the eyes of some are drawn to the increase in interest repayments which occurred between 2002-2008 and 2009-2010. But there are some very important differences between those periods today.

During those periods wages growth was high, the unemployment rate was trending down quite strongly, inflation was far lower than it is today and economic growth was generally very robust.

The Takeaway

While its still plausible that Australia may avoid a recession due to some form of external event coming to the economy’s aid, whether it be from an outsized Chinese stimulus or some event that most of us haven’t yet foreseen, the path to avoid a recession on domestic factors alone is “narrow” to quote the RBA.

Unlike in previous cycles such as 2002-2008 and 2009-2010, there is no strong real wages growth to come to the rescue of households. Instead they are going backwards at the most rapid rate in over 30 years and the essentials of life are consuming a greater proportion of household budgets.

Meanwhile, households have experienced the largest relative increase in mortgage rates in Australian history, more than double the magnitude of the previous record high. Throw in the prospect of fixed rate mortgage holders seeing their interest repayments roughly triple or more, and we’ve got a whole lot of cash being sucked out of the economy.

While I suspect that the labour market and elements of the consumer spending may hold up for an uncomfortably long time, when the Australian economy finally runs out of gas, its going to find itself in a highly challenging place if there is no ‘White Knight’ riding in from overseas to rescue it with some form of external event.

At that point the consumer spending of those under 55 would have been hollowed out significantly, real wages would have fallen to levels last seen 15 or more years ago and whatever buffers struggling mortgage holding households had would largely have been expended.

Ultimately, Australia may yet have divine providence smile on its economic fortunes and deliver it from recession, but with a much more challenging backdrop in many ways than 2008, that deliverance coming from domestic sources alone appears to be an increasingly unlikely prospect.

Brief note: After recent messages of support and pledges to pay a monthly subscription, Substack subscriptions have been turned on at $10 AUD per month and $100 AUD per year. All content will remain free, but if folks want to choose to support my content in this way they can and that would be greatly appreciated.

— If you would like to help support my work by donating that would be much appreciated, you can do so via Paypal here or via Buy me a coffee. Regardless, thank you for your readership.

If you would like to support my work on an ongoing basis, you can do so here via Patreon or via Paypal here

Excellent article, Thank you. Recession or not VERY TOUGH times coming up. my take is the cost of power will have the biggest impact on families after the mortgage train wreck.

Really great analysis Tarric. Love your work and what you share on twitter too.