Chinese Property Sector Death Spiral

The Implications Of A Terminal Decline In China's Largest Growth Engine

As the Chinese property industry continues to slowly deteriorate, the path sentiment of investors toward the sector has come to resemble a rollercoaster ride. The overall trajectory of the real estate construction industry has clearly been in one direction for some time, down.

But when it comes to investor sentiment, its a world of ups and downs, driven by headlines of actual stimulus, rumours of intervention and Pavlovian hopes that bad data will eventually force Beijing to support the real estate construction industry, as they have in the past.

However, like a real life rollercoaster, the path is entirely cyclical and every run through is at its core more or less the same.

As things currently stand at the time of this article being written, there are hopes that the next round of stimulus will finally turn things around for the industry, even though these hopes have been forlorn in over half a dozen instances in the recent past.

Behind the headlines, the reality facing the Chinese property sector is more clear cut than ever. Without a Olympic Gold Medal winning backflip by President Xi and the other members of the senior leadership, the sector is stuck in a downward spiral from which it cannot escape until it meets the fundamental underlying demand for new homes or the much hoped for intervention finally comes.

Fundamental Demand For Homes

In recent years various analysts and academics have attempted to estimate the number of homes in China that are sitting empty. While the figures for these estimates vary quite widely, a range of 65 million to 80 million empty homes has become the go to ballpark range.

In a recent event in the Chinese city of Dongguan, the former deputy head of China’s National Statistics Bureau shared his perspective on how many empty homes he believed there currently are in China.

“Each expert gives a very different number, with the most extreme believing the current number of vacant homes are enough for 3 billion people.”

“That estimate might be a bit much, but 1.4 billion people probably can’t fill them,” Keng said

Meanwhile, data on the demographic makeup of new home purchasers paints an equally concerning picture of what the fundamental underlying demand for new homes actually looks like.

In a National Bureau Of Economic Research report authored by Kenneth S. Rogoff & Yuanchen Yang, it was found that in 2018, 87% of the buyers of new homes already had more than one dwelling. When put into further context provided by the report that China has an urban home ownership rate north of 90%, it becomes clear how low the fundamental demand for new properties in China actually is.

Meanwhile, the size of the Chinese labour force peaked back in 2015 and has since contracted by over 32 million workers or 4.03% of its all time high. Suffice to say that the peak in demand for new residential property in China is in the rear view mirror.

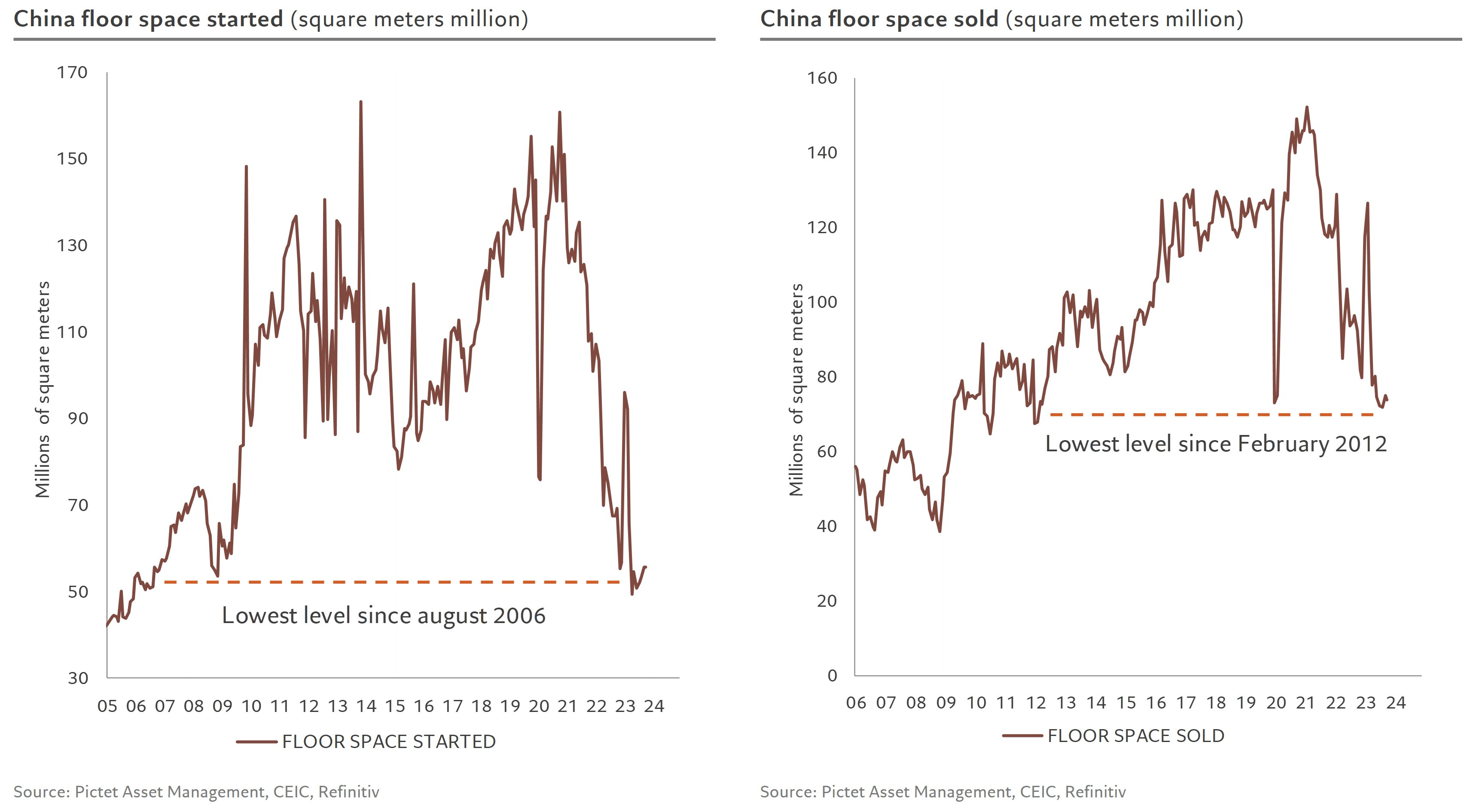

In terms of the amount of floor space started for construction this year, as of the latest data which covers to the end of October, this metric has fallen by 57.4% compared with its peak recorded in 2019.

However, due to the remaining pipeline of projects, the overall fall in fixed asset investment in real estate has been significantly lower. Based on the cumulative spend on fixed asset investment in real estate in the year to date (end of October), overall spending is down by 14.5% compared with its seasonal 2021 peak.

Its here that a very much key but somewhat overlooked point needs to be made.

In past economic cycles property developers were more than happy for construction to immediately follow or even proceed the sale of real estate units in aggregate. But since 2022 that has changed dramatically. Today floor space where construction has just started is significantly lower than the amount of floor space that has been sold.

The gap between floor space sold and floor space started has expanded, from near parity during 2021, to around 20 million square metres per month as of the latest data.

This arguably indicates that the real estate sector is attempting to maintain a reasonably robust backlog of work for as long as humanly possible, knowing that far tougher times lay ahead in the long run as existing projects are completed and the overall remaining pipeline of work dwindles.

Given the possible options, this is arguably the best of a bad bunch of strategies and provides them with more of a glide path down facilitated by this backlog of work, rather than continuing to maintain a higher tempo of activity and then encountering a brick wall of collapsed levels of activity.

Signals And The Rollercoaster

Despite the real estate sub-indices of the Hong Kong and mainland Chinese stock exchanges recently plumbing new loans, some commentators and commodity markets continue to see green shoots and the strong possibility of adequately strong intervention by Beijing on the horizon.

As the rollercoaster analogy alludes to, this has all happened before and will probably happen again.

But the signals provided by the Chinese property sector are painting a very different picture. By attempting to build up a pipeline of future projects, even as elements of the market temporarily bulls up on the sectors prospects, its clear that at least elements of the real estate construction industry is digging in for the long haul.

At the current rate of deterioration its going to take years to approach an equilibrium between underlying demand for new property’s and the construction capacity of the property sector.

Given the ongoing deterioration of the broader wellbeing of private sector developers and land sales by local government being increasingly dominated by state owned developers, its clear which way the winds are blowing.

If intervention on a grand scale is not forthcoming, it will be survival of the fittest for the remaining private sector developers, as the stealth nationalisation of the property sector sees the capacity balance between the two tilt heavily toward the state.

The Outlook

In the short term, the impact of developers building a backlog of projects is a bit of a wash, due to Beijing and provincial authorities doing what they can to fill the gap.

But in the longer term, as Beijing’s resources are needed elsewhere and local governments increasingly find themselves running out of rope, there will be a gradual but significant decline in demand for commodities linked to the property sector, that will only worsen with time and China’s deteriorating demographics.

Taking a look at the issue all the way to a long term time horizon, it also means a deterioration in demand could happen significantly sooner than if projects were pursued and capacity utilization maximized.

On a marginally more positive note, it may also mean that the sector doesn’t hit a brick wall in terms of declining demand and instead may have a more managed glide path.

But make no mistake, if the capacity and activity level of the property sector is allowed to find equilibrium with fundamental underlying demand, it would be very messy for the economy and for the nation’s and companies that rely on the Chinese property sector for their prosperity.

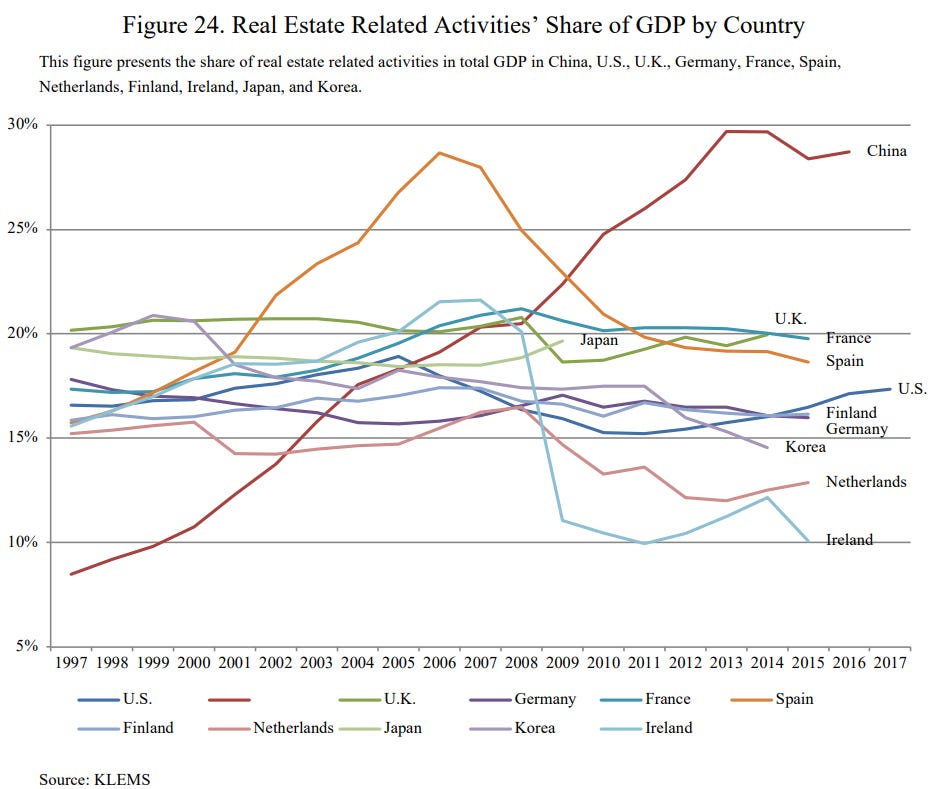

One cannot simply have a sector that contributes to almost 30% of all China’s GDP have its activity level more than halve without serious repercussions.

As by far the world’s largest exporter of iron ore and coking coal, Australia is uniquely exposed to a downturn in the Chinese property sector, even if Beijing manages to somehow conjure an amazingly fortuitous soft landing in the other parts of the economy. I previously covered Australia’s reliance on China in great detail here.

Ultimately, Beijing appears set to try and fill the gap with increased infrastructure spending and support for the manufacturing sector for as long as is reasonably possible. This is clear from looking at the ongoing rise in local government and central government bond issuance, even as concerns over local government debt levels continue to grow with each passing month.

However, between the aforementioned local government debt issue and other priorities, the amount of time Beijing’s support can not only be maintained but consistently increased is limited. If my theory is correct, this is not a scenario that will play out in months, but over years, perhaps over half a decade to fully take its course.

In time, reality will no longer be able to be denied and the enormity of the hit from the bursting of the Chinese real estate construction bubble will become self evident. Unless of course Beijing blinks, throws caution to the wind and attempts to reflate the bubble in a panic, which can never be ruled out.

— If you would like to help support my work by making a one off contribution that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Regardless, thank you for your readership and have a good one.

I am not sure if this has come across your feed. Chris Bloomstrand of Semper Augustus has dropped his yearly letter, it is a 147pg read (great for me as a Berkshire investor) he has included an interesting in depth breakdown (from an investor) on the China outlook going forward. The China Syndrome starts at page 66. As you have related in a couple of other posts, Australia and China are tied due to the resource sector. Thank you for your continued work. Martin

Don't forget the Belt and Road initiative. Chinese are taking their technology and materials across borders. If we had any sense, we would be getting them to construct half a dozen a modern coal fired electricity plants on our coalfields to take advantage of the grids that already exist. That initiative would be seen as an ice breaking venture to put the relationship on a better footing. And a few multi story towers in each capital city. They do them so well.