Government Pumped Housing Prices Before The Fall

Surge in government intervention in the market pre-budget

When the Albanese government implemented its expanded 5% deposit, government backed mortgage scheme in October 2025, it triggered a major surge in first home buyers into the scheme, pushing them into an already overheated market.

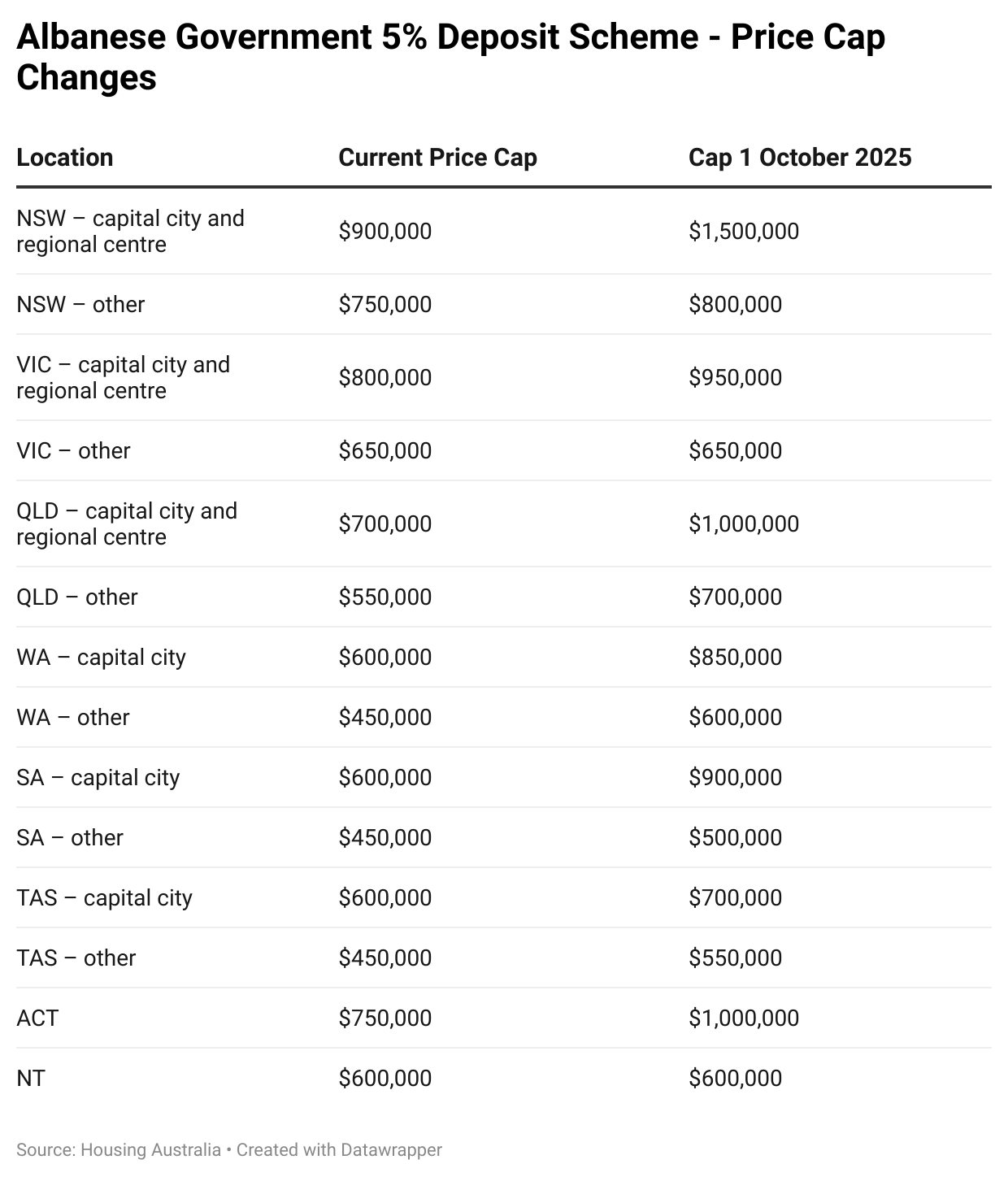

Prior to the Albanese government’s changes, there were two major differences to the 5% deposit scheme we now have today, price caps were lower and there were income caps that needed to be met in order to qualify.

The Albanese government removed the income caps, allowing all prospective first home buyers to access the scheme, rather than the previous cap of $125,000 per year for singles and $200,000 for couples and other joint applicants.

Meanwhile, price caps were raised, in some cases dramatically, with the cap for Sydney and regional centres in NSW increased by $600,000.

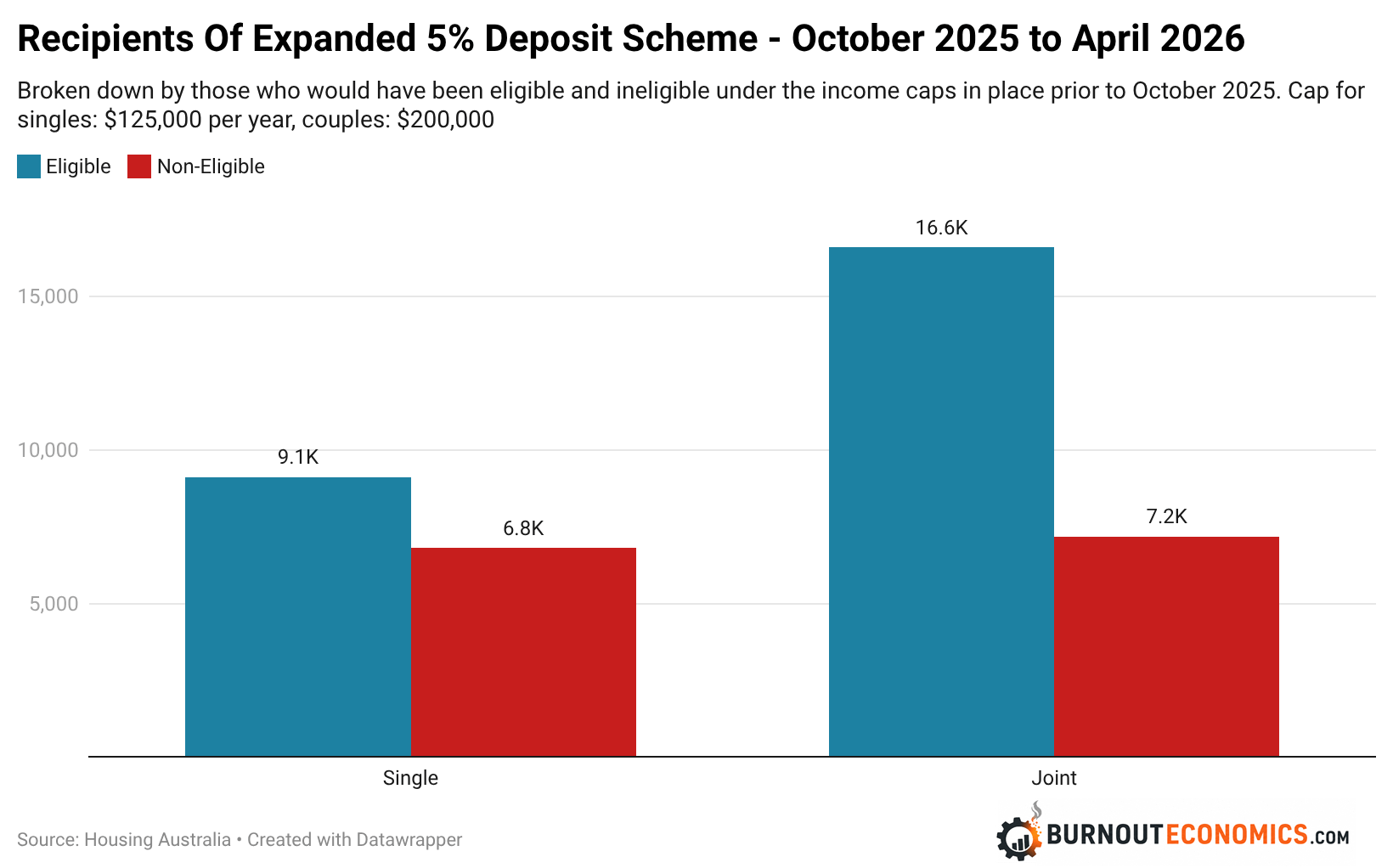

While we lack data on how much the increased housing price caps for the scheme impacted demand, what we do know from figures provided by Housing Australia to a recent Senate Estimates hearing reveals that the level of demand facilitated by the removed income cap is significant.

Of the 39,700 mortgages underwritten by the federal government as part of the scheme between October 2025 and the end of April 2026, 14,000 are from borrowers whose high incomes would have precluded them from qualifying under the previous rules.

Or put somewhat differently, the changes to the scheme solely as they relate to the income caps brought about an increase in demand of over 80% of what it likely otherwise would have been.

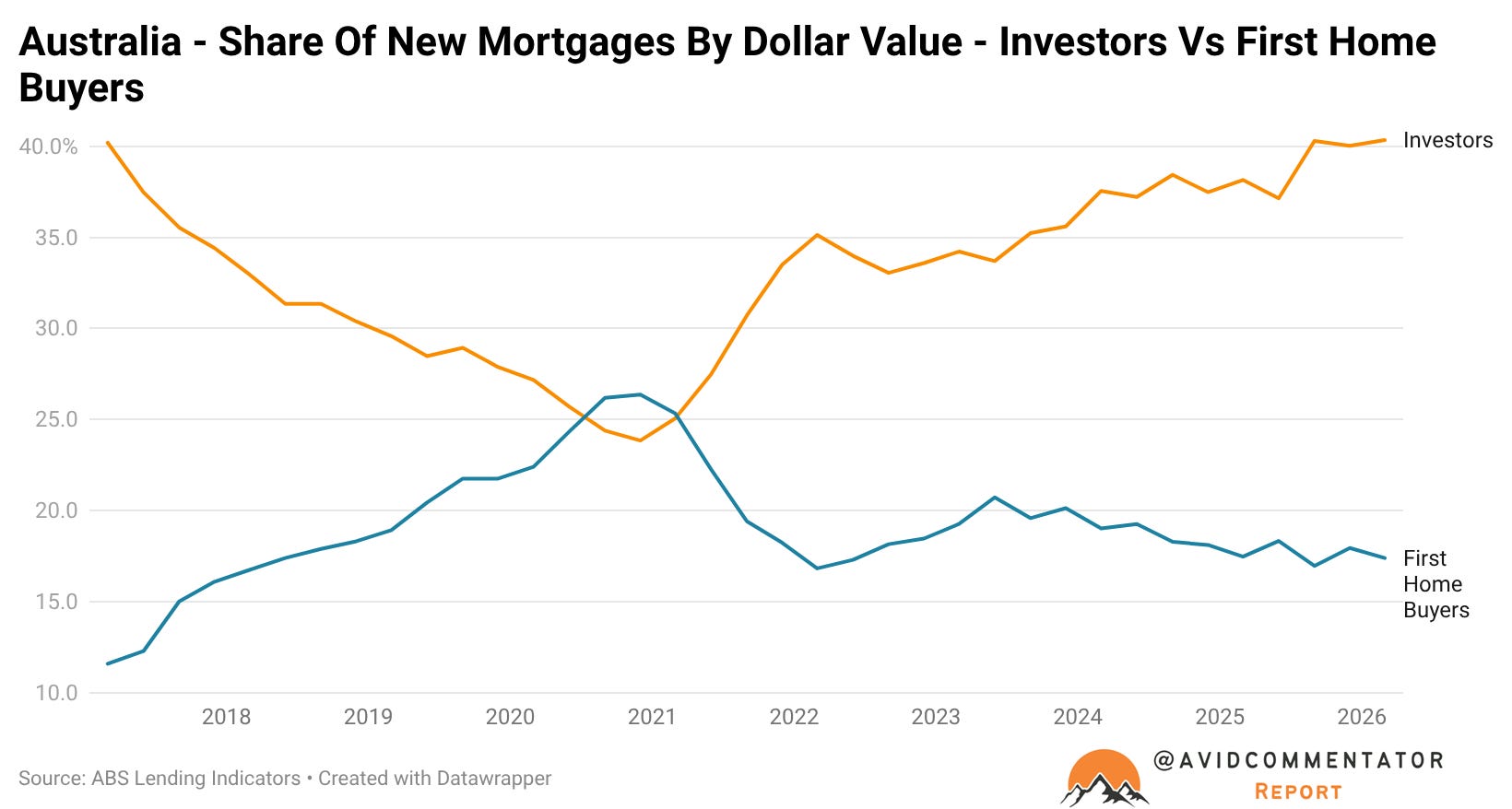

Meanwhile, the announcement that the scheme would be expanded (but prior to its formal introduction) saw the share of demand from property investors propelled to the highest level since 2017.

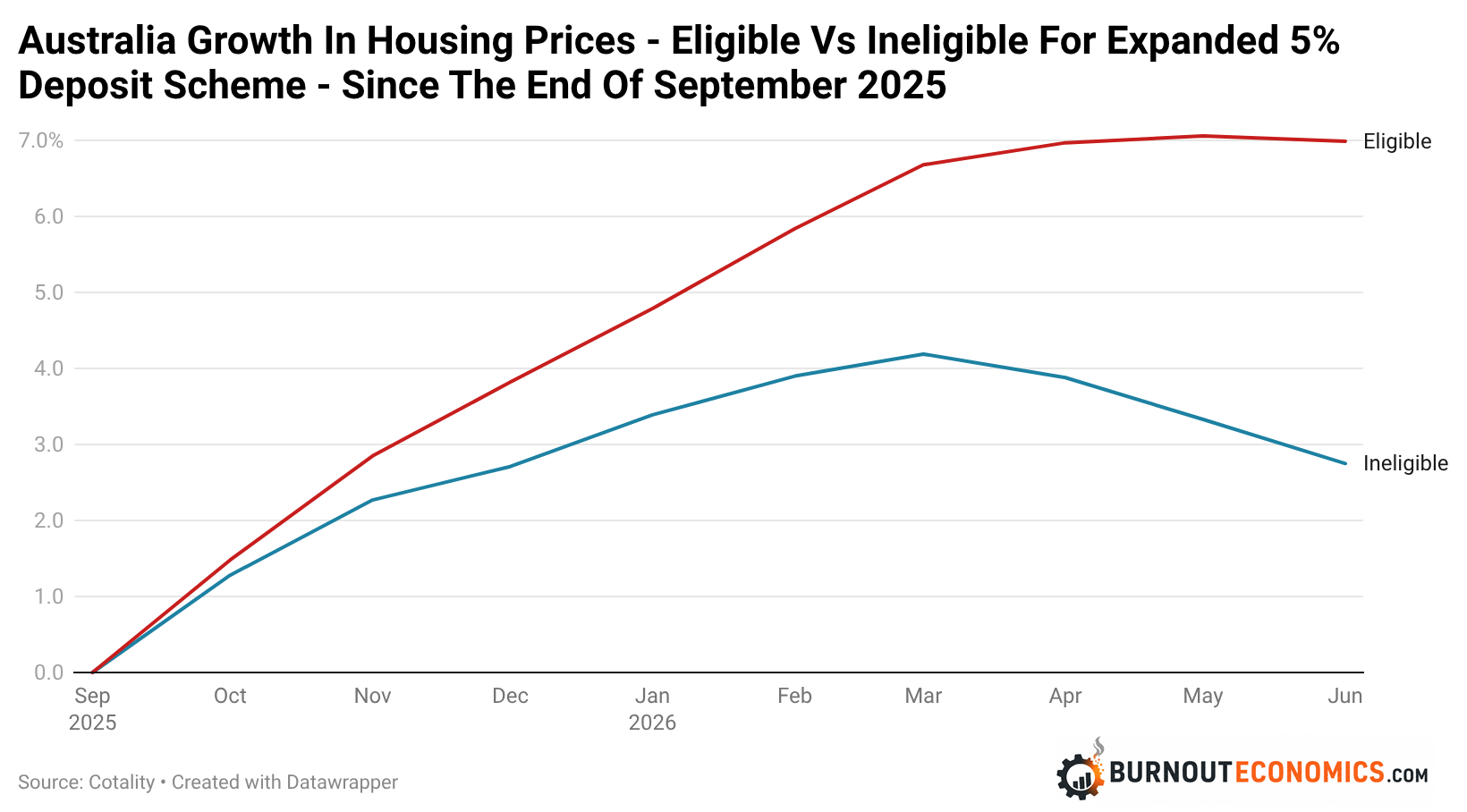

The story that then unfolded is a common one in the history of government intervening in the housing market, the expanded 5% deposit scheme and investor demand boosted prices in the market segments under the price caps.

As the chart below illustrates, the introduction of the scheme was a major divergence point for the two market segments, with prices rising far more strongly in the elements that were eligible for the scheme, while rising significantly slower and falling earlier in the segments that were ineligible.

Between the final data point prior to the scheme’s formal introduction in October to the end of June, eligible properties cumulatively rose by 7.0%, while those were ineligible have risen by 2.75%.

The Takeaway

Based on figures from Housing Australia and the ABS, between October 2025 and March 2026, roughly 55.7% of first home buyer loans were written using the Albanese government’s 5% deposit scheme.

This also doesn’t factor in other government backed loan programs which provide a far smaller but still statistically significant level of support for first home buyers.

In short, prior to the federal budget the Albanese government had become the driving force behind a majority of first home buyers into the housing market.

In a vacuum this isn’t an awful idea, the Menzies government employed a thematically similar scheme in the 1950s and 1960s, to great success.

But into a heavily under supplied market defined by extremely strong demand from property investors it was a recipe for only one thing, higher prices.

Now housing prices are falling, the scheme is increasingly seen in a different light, as a potential driver of households into negative equity.

If the government genuinely wanted to raise home ownership rates, it would better balance overall supply and demand, while moving to limit demand from property investors for existing homes.

Instead it has pursued a strategy what is effectively boom followed by potential bust, amidst a backdrop of a rental crisis that is crushing household formation.

Ultimately, its hard not to treat with the Albanese government’s housing policies with at least a high degree of skepticism.

They are on one hand taking away from demand with the changes to negative gearing and the capital gains tax changes on existing homes.

But on the other they have spent over four years propping up the market with high levels of migration, support for investors through the ongoing rental crisis and various changes to boost demand from first home buyers through various government programs.

— If you would like to help support my work by making a one off donation that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Thank you for your readership.