The Most Burning Question Answered: When Could Australian Interest Rates Be Cut?

By how much? And how would that effect mortgage repayments?

Brief Housekeeping: This article is a bit of a preview of what will be on offer for paid subscribers (and existing Patrons as of this date) later in the new year. Longer articles (shorter versions still available for free subscribers), high resolution chart packs, articles in downloadable PDF form (links below).

This is part of the ongoing drive to be able to dedicate more time to my independent content creation.

Since the RBA first began raising interest rates a little over 18 months ago, the burning question on the minds of many commentators and on the lips of mortgage holders has been, when are interest rates going to be cut?

Looking back on the course of the RBA’s cash rate since November 2011, its understandable why. Between November 2011 and November 2020, the RBA slashed the cash rate from 4.75% to 0.1%. But more than that, during the pandemic they also implemented yield curve control and provided $188 billion in funding to the banks at a cost of just 0.1% per annum, facilitating the average 3 year fixed mortgage rate falling below 2%.

In the years since the pandemic lows in rates, the 30 year illusion that the trend in interest rates would always be down has been shattered, with the RBA engaging in the largest relative rate rise cycle since records began in 1959.

Based on the average payable variable owner occupier mortgage rate, mortgage interest repayments have risen by a 126.9% since their early 2022 lows. The largest ever prior increase in interest repayments in a single rate rise cycle based on the average benchmark discount variable rate was 58.5% between 2002 and 2008.

But that occurred over an almost 6 year period, which gave wages growth, which was highly robust at the time a chance to catch up. Meanwhile, the current cycle has played out over just 19 months.

When Could Rates Be Cut?

Based on historic rate cut cycles over the last 50 years, the average time between the peak in mortgage rates and the RBA cutting rates is 9.8 months. Excluding the rate cut cycle of 2008, which was precipitated by the Global Financial Crisis (GFC), the average time is 10.6 months. Assuming that we don’t see a rerun of GFC like event and there are no further rate rises, that would theoretically put rate cuts around September next year.

Over the last 50 years the longest rates have been kept at their cyclical peak is 17 months. In short, once rates hit their peak its only a matter of time before inflation is adequately tamed for them to be dropped or the economy has taken a big enough hit to justify loosening monetary policy.

What Have Conditions Looked Like Historically?

After spending much of the last three decades talking about the importance of their 2-3% inflation target, there is a rather widespread perception that headline inflation needs to at least be within that target range before rates are cut.

But based on the state of headline inflation when large scale rate cut cycles kicked off in the era of the 2-3% target, this has actually never been the case. Of the four major rate cut cycles of this era, starting 1996, 2001, 2008 and 2011, the average rate of headline inflation was 4.43%. If we exclude the 2001 data point which is distorted higher by the introduction of the GST, the average comes down to 3.87%.

If we take a slightly different tack and use the trimmed mean as our preferred metric, then things are quite a bit different. The average level of inflation at the time of cuts comes down to 3.13%.

If we use the RBA’s own forecasts as a guide to when we could reach these historic trigger points, CPI inflation is expected to come in under the historic average level for cuts by H2 2024 and the trimmed mean hit below its version of this metric by the first half of 2025.

Ultimately, while the broader state of inflation matters to the RBA’s cutting process, when push comes to shove as the economy slows or a crisis arrives, it takes a back seat to other considerations.

This is something that the RBA has gained a reputation for with analysts and the bond market, it is well known that it puts a far greater emphasis on the state of the labour market and the economy (see also housing market) than the Fed and many other central banks.

The inclusion of the historic average levels of inflation at rate cuts is not intended to provide a concrete line in the sand at which the RBA may feel it is appropriate to act. But to instead make it clear that the RBA is not absolutely committed to its inflation target. And that it can and will cut rates if it feels other factors are compelling them to do so.

There was some sign of growing concern about the labour market in the RBA’s December meeting minutes.

“there is the possibility of a larger rise in the unemployment rate than anticipated.”

The Fed Factor

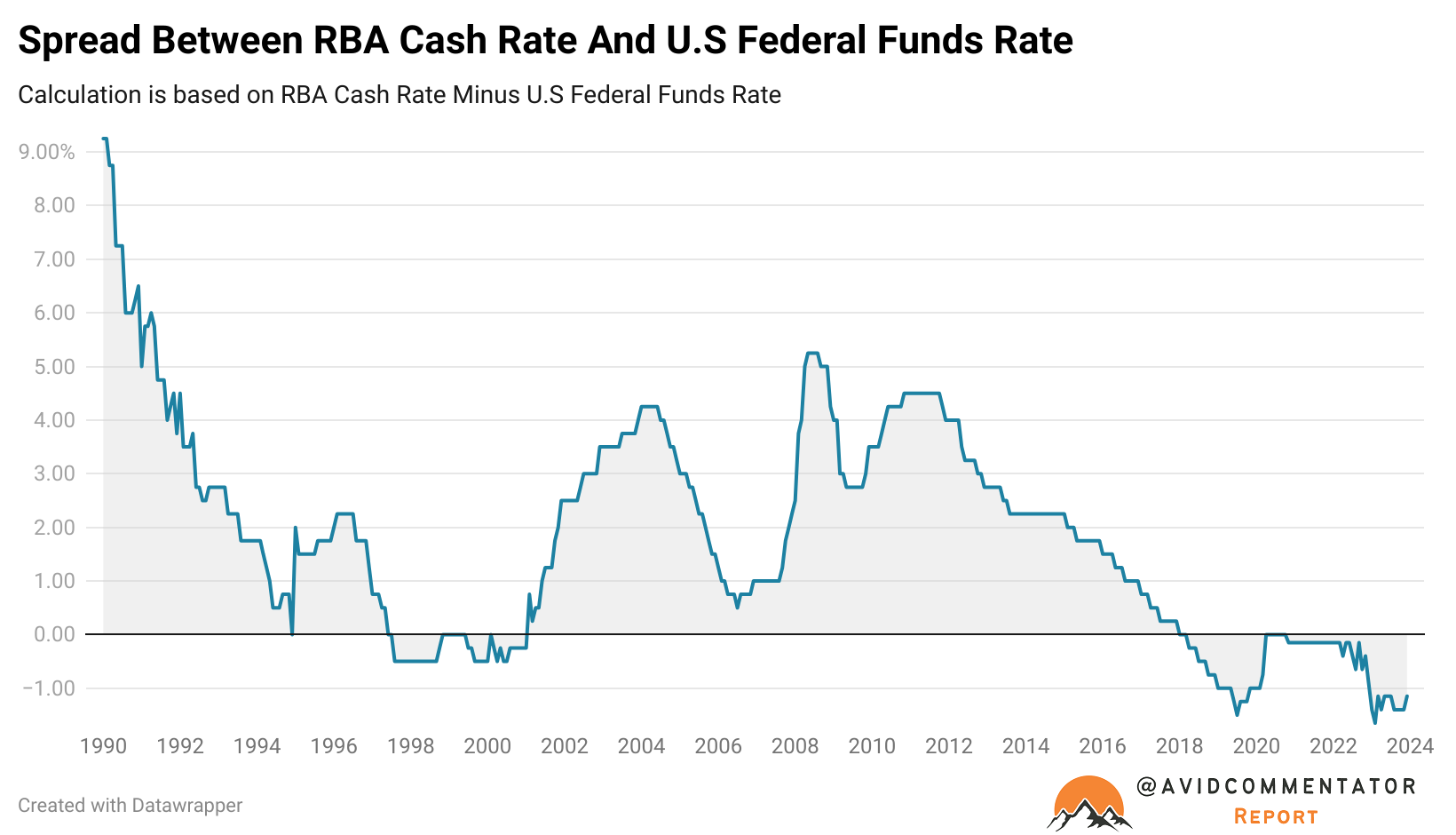

Of the five major rate cut cycles of the cash rate era (1990 onwards), three were either pre-empted by the U.S Federal Reserve cutting rates or there was a clear signal that the Fed was highly likely to cut rates at their next meeting.

Of the remaining two where the RBA went it alone, its immediately clear why the denizens of Martin Place why they felt they had the scope to act unilaterally. When the RBA cut rates in January of 1990, the RBA cash rate was 9.25 percentage points higher than the Federal Funds rate. In the other instance in November 2011, the cash rate was 4.5 percentage points higher than its U.S equivalent.

Its worth taking a step back for a moment here and examining the longer term relationship between U.S and Australian central bank interest rates. For the overwhelming majority of the last 34 years, the RBA cash rate has been higher than the U.S Federal Funds rate. In the early part of that period, far far higher.

Over the time period covered by the cash rate era (starting January 1990) through to the start of the pandemic, the average spread between the RBA cash rate and the U.S Federal Funds rate was 2.12 percentage points in the RBA cash rate’s favour.

If we expand the timeline to encompass the years during and since the pandemic, the spread does tighten somewhat, but remains an average of 1.81 percentage points in the RBA cash rate’s favour.

This illustrates nicely that the cash rate sitting significantly lower than the Federal Funds rate is not the historic norm, with the RBA historically being significantly more aggressively pro-active than the Fed during the post-Volcker years.

When Could The Fed Fire The Starting Gun?

Following Powell’s recent dovish remarks and a growing range of viewpoints emerging from various senior Federal Reserve members, several major investment banks have begun pencilling in cuts for as early as March (Goldman, BofA).

As of the writing of this article, CME’s Fed Watch tool is pricing in a 68.8% of a cut in March and 95.8% chance of a cut in May (from current Federal Funds rate).

Its going to be interesting to see how bond market pricing evolves on the timing of cuts, as some senior Federal Reserve members push back on the idea of rate cuts so early in 2024.

We have seen some absolutely huge swings in the bond market in recent months, so it would not be at all surprising to see a bounce in yields, particularly as postponed long bond issuance resumes in the new year.

RBA Rate Cut Pricing

The market pricing of the RBA’s future rate moves has also moved aggressively in line with what has been seen in global markets. Currently the first 0.25% rate cut is fully priced in for July, with a 95.4% chance of rates being cut in June. A second 0.25% rate cut is fully priced in for November. With a third rate cut not fully priced in until June 2025.

Cut By How Much?

Based on sizable historic cutting cycles exceeding a 1.5% drop in mortgage rates, the average reduction in mortgage rates over the last 40 years across each cycle has been 29.3% (based on the benchmark discount variable mortgage rate). However, its worth noting that these numbers are heavily skewed by the rate cut cycle of 1990 to 1993 and 2008 to 2009.

In the early 1990s cutting cycle, the cash rate was slashed from its all time high of 17.5% amidst the highest unemployment rate since the Great Depression (peak of 11.2% in 1992). During this rate cut cycle mortgage rates were cut by the greatest degree on record, being reduced by 48.5%.

The other outlier in the data is the rate cut cycle of 2008-2009, which saw the cash rate slashed by 4.25% in just 8 months, as the GFC sent the global financial system into a tailspin. During this period, mortgage rates were reduced by 42.8%.

Excluding these two instances from the scenario, the 40 year average for a cutting cycle’s reduction in mortgage rates comes down to 22.8%.

As of today, the average payable variable mortgage rate is approximately 6.49%. Based on an average cutting cycle, including those defined by double digit unemployment and the GFC, the average payable variable mortgage rate would come down to around 4.6%. Excluding the two outlier eras from the scenario, the average payable variable mortgage rate would sit at around 5.0%.

In terms of where this would leave the cash rate, the crisis inclusive scenario would see the cash rate fall to 2.45% and the non-crisis scenario would see a cash rate of 2.85%.

Where Does That Leave Mortgage Holders?

Its here that the rubber meets the road and the abstract becomes far more real. In order to provide the most comprehensive and relevant picture to the broadest possible audience, we’ll be using two separate bases with which to assess the impact of falling mortgage rates on the interest repayments of households.

One base will be when variable mortgage rates bottomed out for the cycle in April 2022. The other base will be the end of 2019, the last period before the impact of the pandemic started to be felt in global rate markets.

By taking these two bases and then applying five different rate cut scenarios, we can begin to get an idea of the challenge that mortgage repayments may still present, even after a major rate cut cycle.

Based on the average cutting cycle mortgage interest repayments would be 60.4% higher than the lows seen in 2022, excluding the crisis driven rate cut cycles, interest repayments would be 75.2% higher.

Using late 2019 levels as a base, the 40 year rate average rate rise cycle would see interest repayments 28.5% higher than 2019 and excluding the crisis driven rate cut cycles, this would see the figure 40.3% higher.

Looking Ahead…

Based on what could be considered a ‘normal’ rate cut cycle, the degree of relief on offer from lower rates is likely not going to be in the same ballpark as the current relatively widely held expectations of a return to a crash dive in rates.

However, if the domestic and/or global economy deteriorates to a more significant degree than seen in prior non-crisis rate cycles, then far greater cuts may be on offer. But unless economy’s worsen more significantly than the average prior cycle, its challenging to see the RBA returning the cash rate to even its pre-pandemic low of 0.75%.

That being said, a domestic and/or global recession brings its own long list of problems, which may end up being significantly more challenging for households than the temporary difficulties presented by higher interest rates.

As for my own view, I see the RBA cutting rates during Q3 at the latest. Given the extremely high rate of labour force growth, the Australian labour market remains significantly more exposed to a swift rise in unemployment compared with its American counterpart.

So far the Australian labour market has been remarkably resilient, but as the broader economy slows, this can’t continue forever. In a recent note CBA warned that:

“A ‘nowcast’ of Q4 23 GDP suggests we may see an outright contraction in GDP over the quarter."

Ultimately, its all a bit throwing darts at a dart board a year in advance given the variables. A crash dive in rates is a possibility, but if it were to occur amidst GFC-esque conditions and the first real Australian recession in 33 years, then mortgage holders may end up wishing they never got the rate cuts they so desire.

On the other hand, a more average rate cut cycle may only see moderate relief and a continued struggle with mortgage repayments and hard hit real household incomes baked in for at least several more years to come.

PDF version of this article: Link

High Res Chart Pack: Link

— If you would like to help support my work by making a one off donation that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Regardless, thank you for your readership and have a good one.

Excellent thank you.