The World Of $286 A Barrel Oil

The reality of physical oil markets

In recent days a mood of calm has descended on markets, with the S&P 500 recently trading at record highs and oil back under $90 a barrel.

For some on social media it is enough to declare that the only way is up for equity markets and that the “Nothing ever happens” crowd has once again emerged on top, yet out in the world of physical oil things could scarcely be more different.

According to HSBC CEO Georges Elhedery, a Sri Lankan importer recently paid $286 a barrel for oil.

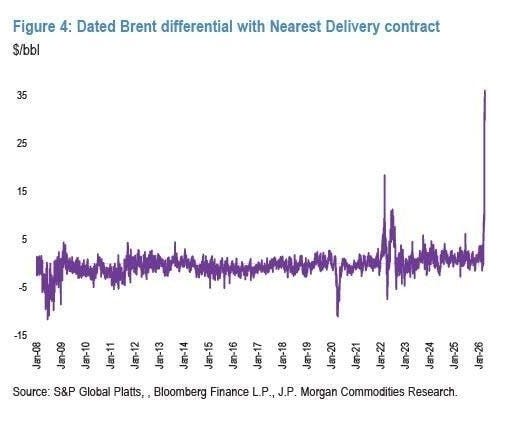

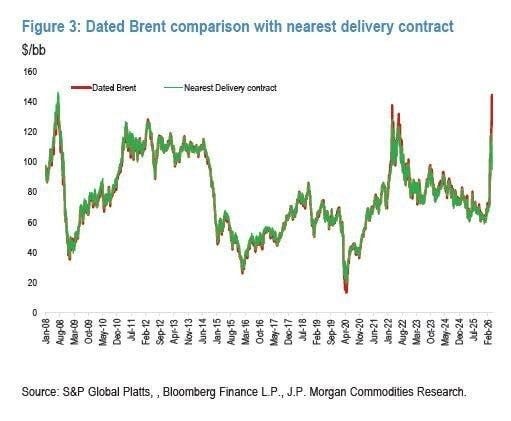

The performance of shorter term proxies for physical oil delivery and dated contracts is vastly different.

This is illustrated nicely in the chart below from S&P Global Platts, the gap between the price for Brent crude is around $35 a barrel, a completely different world to the normal spread between dated Brent and the oil price for the next futures contract.

As the chart below indicates this is a deeply abnormal set of market circumstances.

In the words of FT Alphaville editor Robin Wigglesworth in a recent article:

“This is pretty strong evidence of a distressed physical energy market, with the stresses particularly acute in Asia”

A Reality Check

Simply put, there is a growing gulf between the perception of the oil futures market and what importers and traders are actually paying for oil in the physical world.

This is something that HSBC CEO Georges Elhedery recently went into detail on in an interview with the U.K Financial Times.

“What worries me is not the headlines. I mean, oil headline is above $100, $110. Realistically, if you are now trying to get oil from the Middle East, you may be paying $140, $150.

Realistically, if you try to get oil from the Red Sea, you are paying more than $30, $40 for shipping. Insurance costs, which used to be 25 basis points, is more like 5%, and war insurance has been scrapped — you’re paying 5% without even the war insurance component.

So the barrel of oil door to door or the barrel of refined oil door to door is way above the headline price of oil.”

These are the challenges in the oil market in the here and now.

If the crisis continues into the coming weeks and months, which will intensify as exports of Iranian oil filter out of global refining chains, then the situation will only become more desperate.

As nation’s attempt to secure oil and fuel in what is quite literally an existential struggle for the state of their economy’s, they will continue to accept higher and higher prices until they simply can’t afford to pay anymore.

This is ultimately how we arrive at up to 13 million barrels per day of demand destruction to balance the market on a long term basis.

To put this into perspective, at the absolute height of the pandemic in early 2020 peak oil demand destruction was 15 million barrels with much of the world in de-facto or literal lockdown.

Keep reading with a 7-day free trial

Subscribe to Burnout Economics to keep reading this post and get 7 days of free access to the full post archives.