Australian Stagflation Risks Rocket

Over on my YouTube channel, Martin North and I recently did a full length deep dive on Australia’s fuel supplies and the state of the economy pre-war, that can be found here.

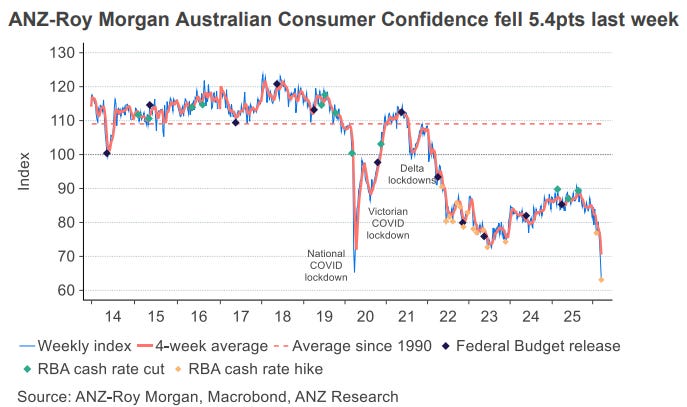

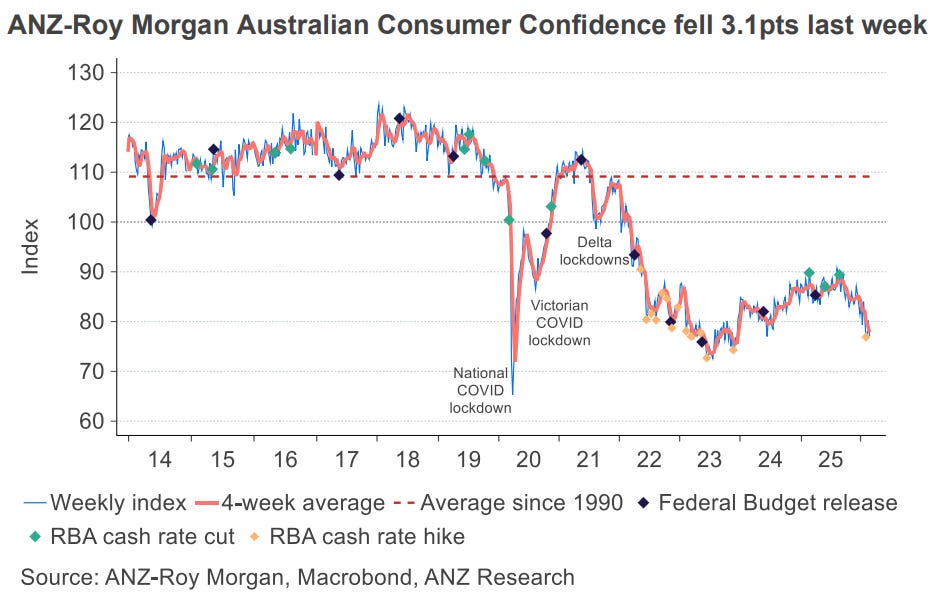

Yesterday morning, the latest ANZ-Roy Morgan consumer confidence survey was released, revealing that the metric had fallen further from already depressed levels to the lowest level since records began 53 years ago.

The news from across the board was less than favourable.

The overall index fell by 5.4 points for the week, to hit a figure of 63.1.

To put this into perspective, the average since 1990 is around 109, with the average since 2001 at 115.

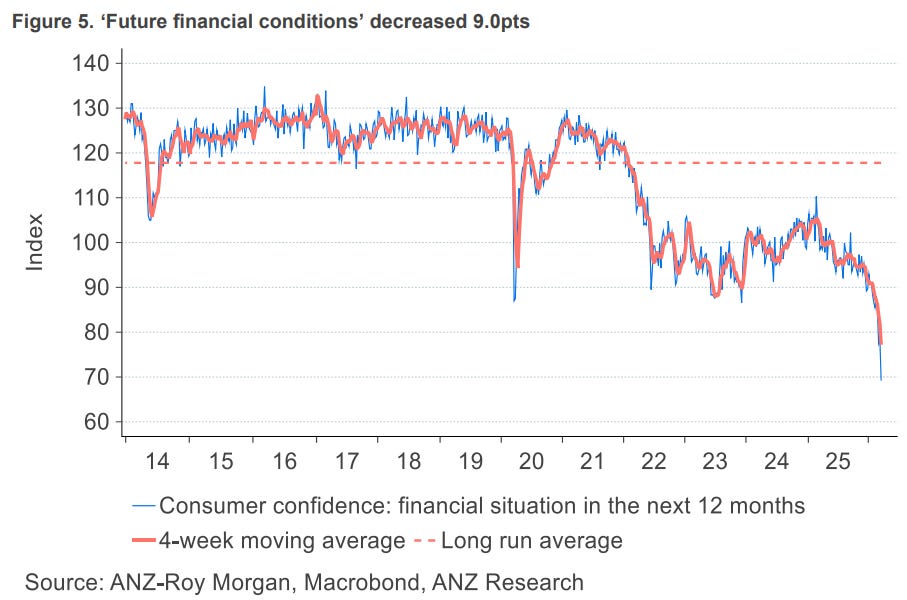

In terms of the outlook of households for their financial situation over the next 12 months, that has fallen to sit dramatically below it’s pandemic era lows.

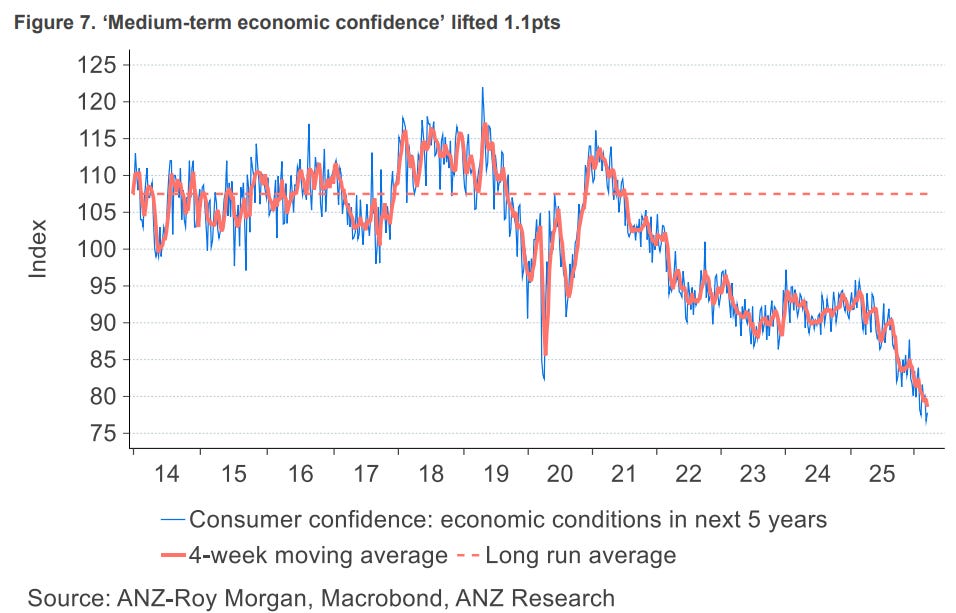

On a more long term basis, the 5 year economic outlook is also extremely poor, but this is also nothing new, with this subindex sitting trending below the pandemic era lows for quite some time.

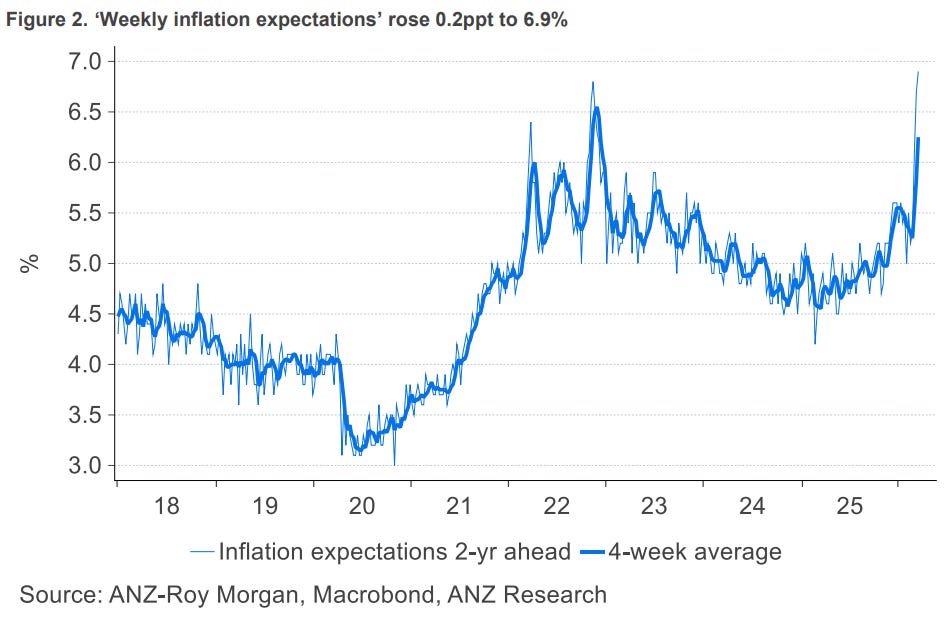

Meanwhile, the inflation expectations of households with a two year time horizon have rocketed to 6.9%, higher than even the absolute peak seen during the pandemic.

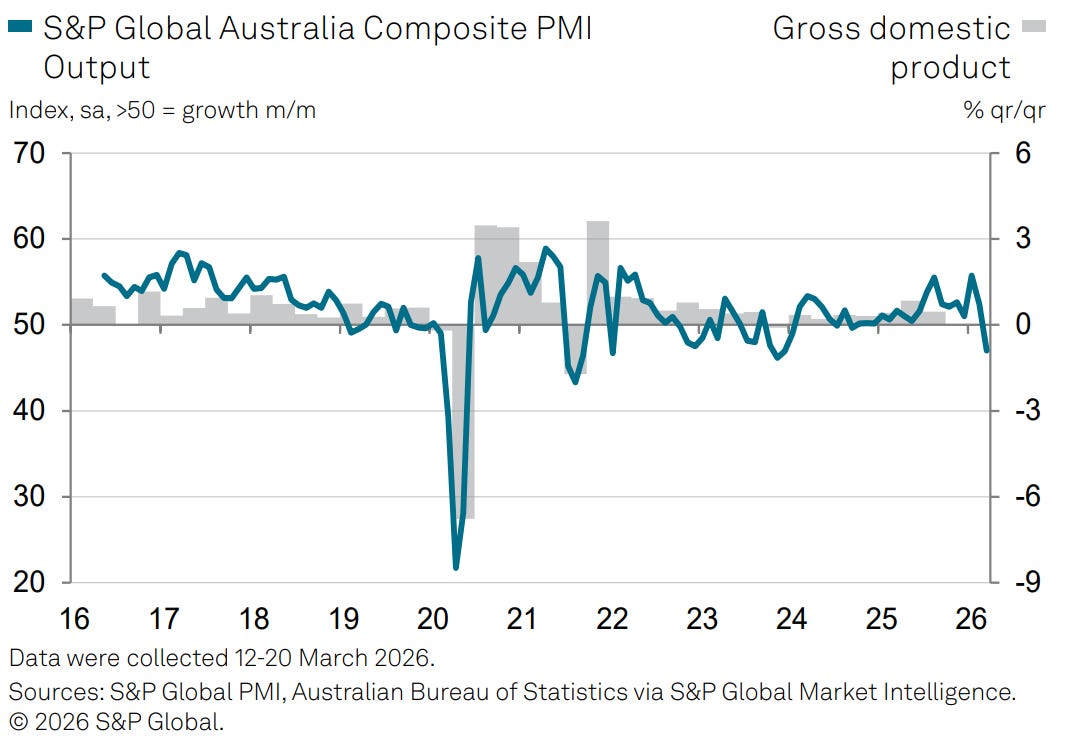

Concerns of rising inflation held by households was swiftly confirmed by the release of the Australian S&P PMI.

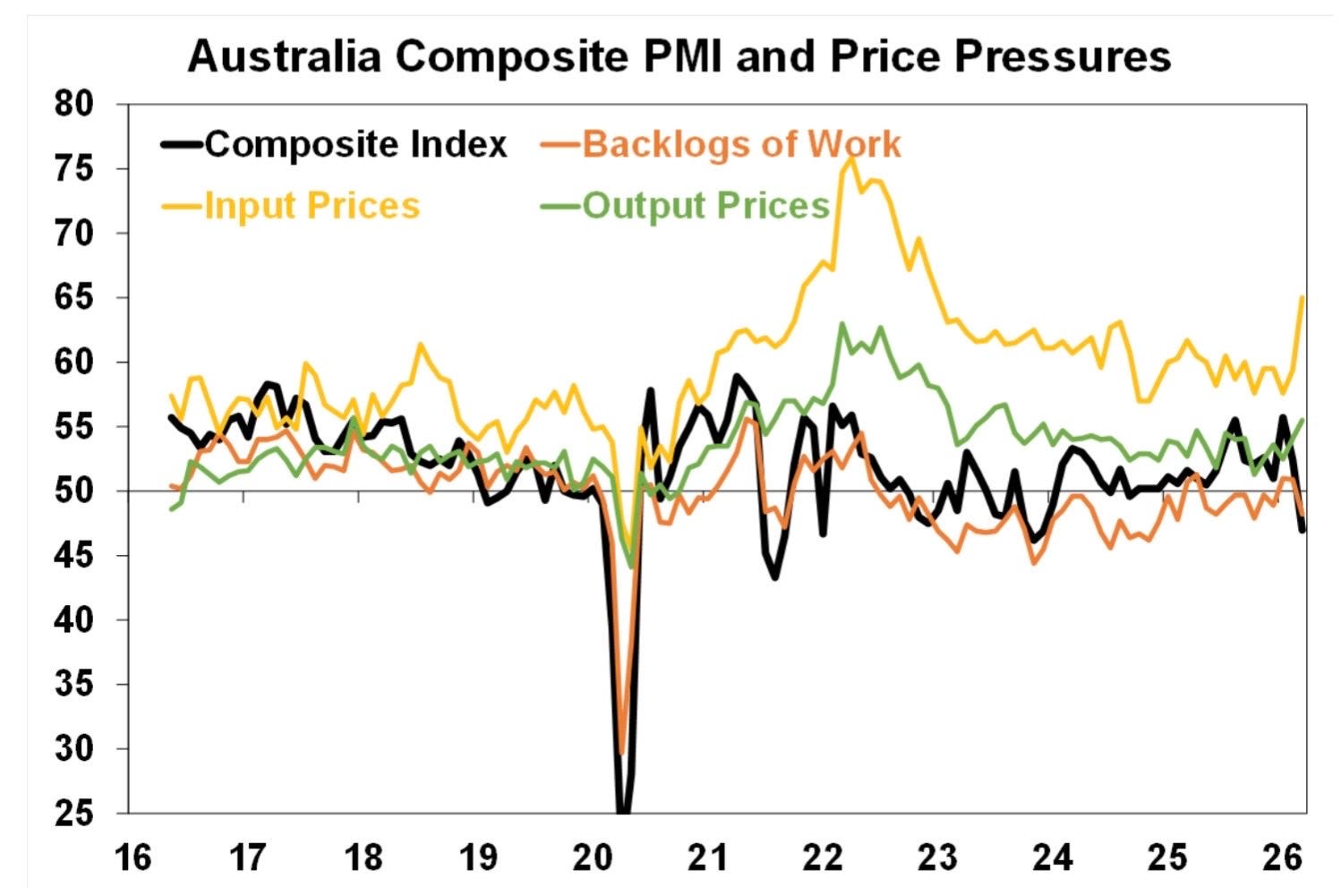

“March saw a steep rise in input prices faced by Australian private sector firms. At the composite level, the rate of cost inflation jumped to its strongest in over three years, with the equivalent reading for charges reaching its highest level since August 2023.”

The rise in selling prices to consumers has also swiftly taken off, with price growth hitting it’s highest level in 31 months.

The broader picture painted by the PMI was also concerning, with the composite measure falling from 52.4 in February to 47.0 in March.

PMI’s are diffusion indexes, with a result above 50 indicating growth and below 50 indicating contraction.

The fall in the services sector was particularly acute, with the subindex falling from 52.8 in February to 46.6 in March.

As the chart below from AMP Chief Economist Shane Oliver reveals, even the limited impact of less than 3 weeks of war (the snapshot was taken between the 12th and 20th of March) has seen input prices rise to the highest level since late 2022.

While the impact of the war of the Middle East is deeply concerning, the reality is things were not in a great place even before the war.

Consumer confidence had been trending down from already well below average levels for over 6 months prior to the war.

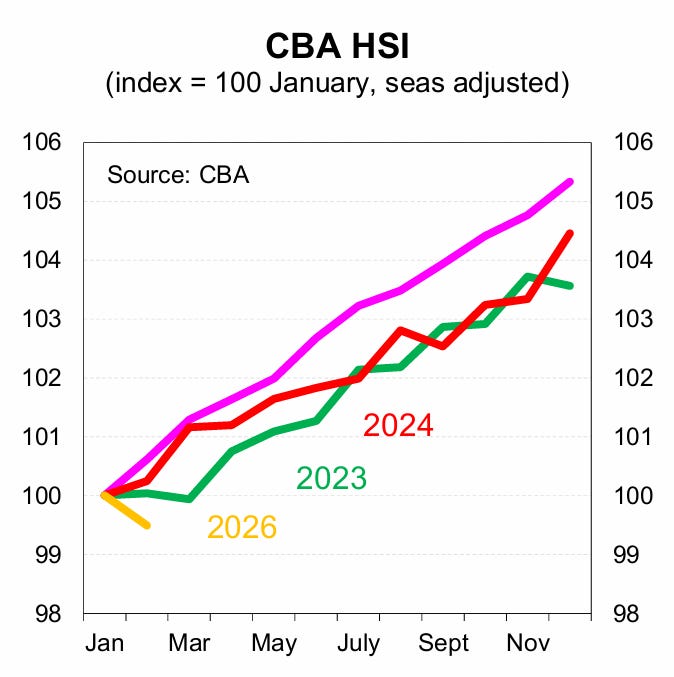

Meanwhile, conditions for households as measured by the Commonwealth Bank’s Household Spending Index (HSI), revealed that even prior to the war consumer spending was contracting at an aggregate level.

On an inflation adjusted per capita basis, the year on year result was also extremely poor, with real spending for outright home owners falling by 3.0%, renters falling by 2.2% and mortgage holders rising by 0.2%.

In short, the growth in the real consumer spending of households on this metric was being driven almost entirely by the expansion of the working age population, which is being driven overwhelmingly by net overseas migration.

The Takeaway

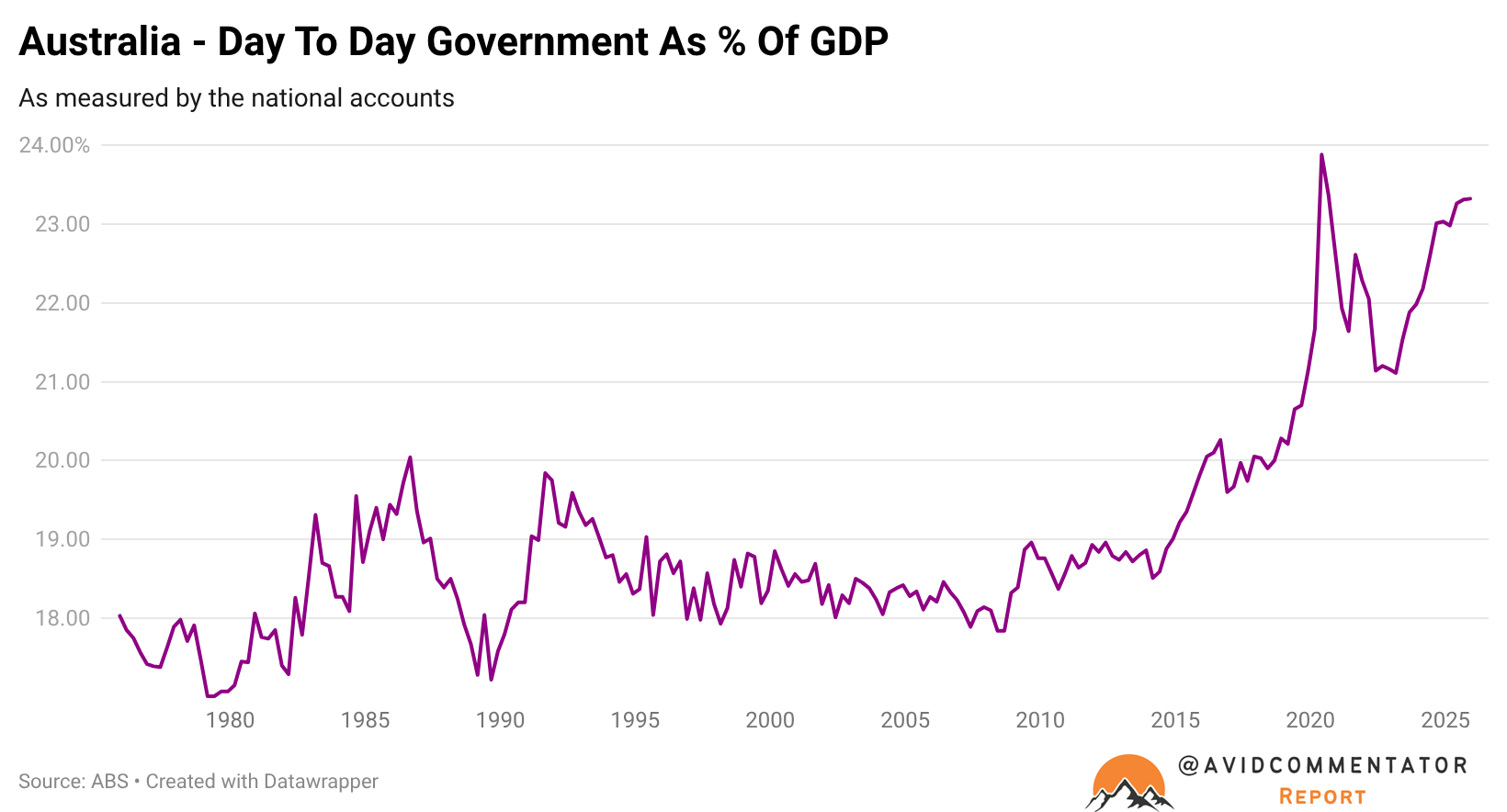

As I have previously covered here at Burnout Economics, the Australian economy is hardly in amazing shape.

It is an economy heavily reliant on the expansion of government as a proportion of economic activity, growth in taxpayer funded employment and high levels of migration.

If for whatever reasons the economy and labour market were forced to stand on their own two feet without that support, a very different picture would have emerged even prior to the war in the Middle East.

Now with the prospect of a global recession and energy crisis looming on the horizon, as well as the possibility of fuel shortages domestically, it has become a perfect storm for a potential episode of stagflation should the crisis not be resolved relatively swiftly.

Ultimately, the outlook for Australia’s future is a deeply concerning one that could very plausibly turn into a bout of stagflation, followed or perhaps even accompanied by a recession.

— If you would like to help support my work by making a one off donation that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Thank you for your readership.

Thank you for your content in these uncertain times Tarric 🙏