Strait of Hormuz Closure Logistics

And is there spare capacity oil capacity to make up for it?

As the war in Iran continues to unfold, I thought it would be worthwhile sharing various data and relevant information that comes into my possession here on Substack.

For those looking for a basic primer on the importance of Iran to energy markets, the importance of the Strait of Hormuz and the potential geopolitical implications, that can be found here.

Today we will be examining two major topics in detail:

If the Strait of Hormuz is effectively closed to civilian transits, can it be circumvented and to what degree?

Is there significant capacity for other nations to make up the short fall in oil production should a large proportion of Middle East output be stranded?

Can the Strait of Hormuz be circumvented?

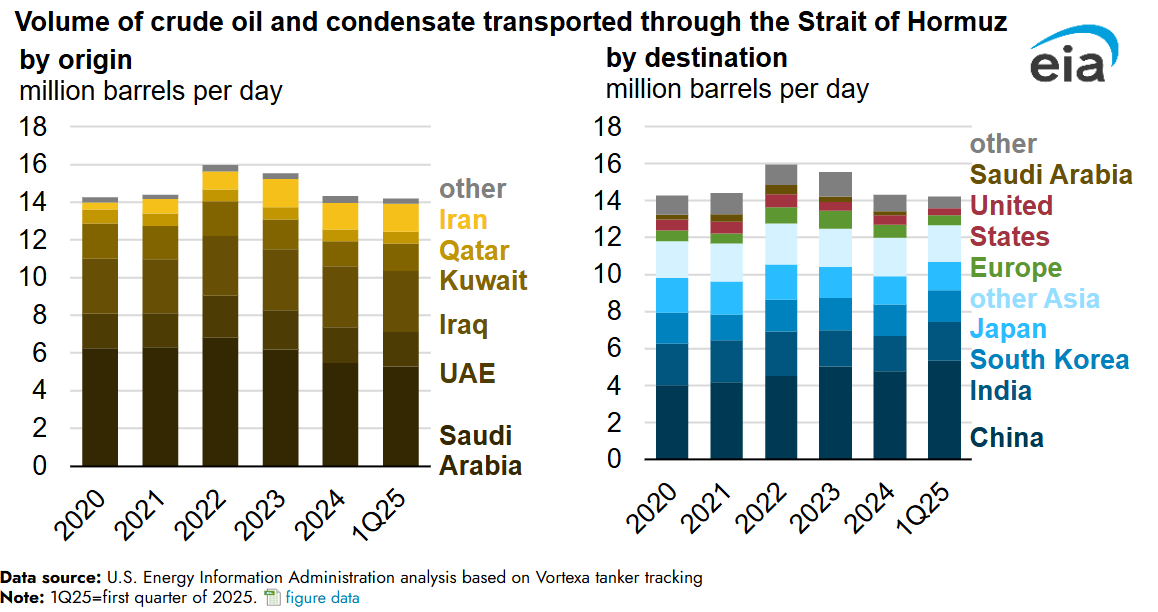

As of the time of the writing of this article, the flows of maritime traffic through the Strait of Hormuz has slowed to a trickle, with getting on for 200 tankers now anchored on either side of the strait waiting to transit once it’s considered safe and appropriate.

For decades a blockade or closure of the Strait of Hormuz has been the nightmare scenario for the nation’s on the Persian Gulf, a means by which the flow of oil, gas and other exports could be strangled off and present a huge military and economic challenge.

For this reason, varying degrees of contingency plans have been put in place by Saudi Arabia and the United Arab Emirates.

For the Saudi’s their strategy rests on the East-West Pipeline (EWP).

Construction initially began on the 1,200km pipeline in 1982, prompted by concerns that the flow of Saudi oil could be impacted by the Iran-Iraq war.

The EWP transports oil from the Abqaiq processing hub to export terminals at Yanbu on the Red Sea.

Source: EIA

According to a 2024 analysis by the U.S EIA, the pipeline provides scope for shipping up to 7 million barrels a day of Saudi production to the Red Sea ports, up from a previous total of 5 million barrels a day following the conversion of a gas pipeline to carry crude.

However, it is worth noting that 1.7 million barrels per day of oil already flows through the EWP and doesn’t count toward the little over 14 millions barrels per day transiting the Strait of Hormuz.

In better news, this represents on paper, a large majority of current Saudi oil exports having a means to avoid the Strait of Hormuz.

However, this also means that the Saudi’s would not have the adequate infrastructure to export their current spare capacity in the event of a protracted crisis, which is estimated to be around 1.84 million barrels of oil per day.

The United Arab Emirates (UAE) has also constructed pipelines to avoid the Strait Of Hormuz.

The Abu Dhabi Crude Oil Pipeline (ADCOP) moves 1.5 million barrels of oil to Fujairah, which is on the other side of the strait from the Persian Gulf and in the Gulf of Oman.

Currently, approximately 600,000 barrels per day transit the ADCOP pipeline, leaving around 900,000 barrels in spare transit capacity.

There is a second pipeline currently under construction also to Fujairah, adding a further 1.8 million barrels per day of capacity for rerouting. It is expected to become operational in 2027.

The existing pipelines held by the UAE provide scope for approximately 54.5% of current total exports to be rerouted.

Iraq does have a theoretical option in the form of the Kirkuk-Ceyhan pipeline to Turkey, which would provide the capability of transferring up to 1.2 million barrels per day, but this route has reportedly been closed since 2023 amidst still ongoing political and legal disputes.

If this was somehow reactivated and fully utilized it would represent capacity to reroute roughly 37.5% of Iraq’s current oil exports.

On the other hand Kuwait and Qatar, lack such contingencies.

Overall, if all the spare pipeline capacity was able to be fully utilized, which is a big if, it would represent up to 7.4 million barrels per day still making it to market despite the closure of the Strait of Hormuz.

If realized that is equivalent to around half the oil transiting the Strait of Hormuz having a secondary avenue to market, if given the time to set up the required logistics.

But the issue unfortunately goes beyond solely oil.

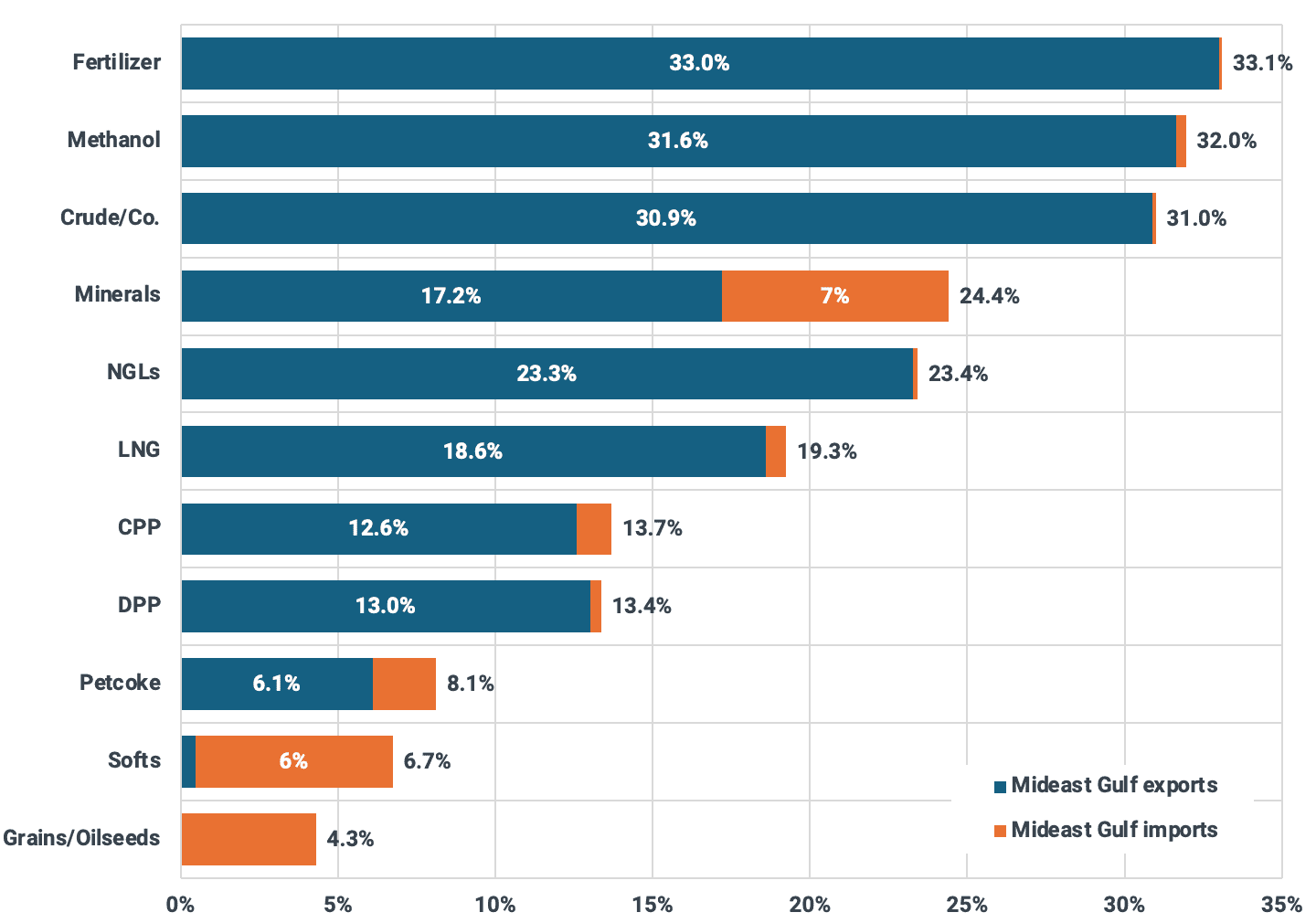

According to an analysis from global trade analysis firm Kpler, 33.0% of the world’s exportable fertilizer flows through the Strait of Hormuz, along with 18.6% of exportable liquefied natural gas (LNG) and 17.2% of global mineral exports.

While fertilizer can theoretically be rerouted overland, it would represent a near impossible challenge to do so, particularly on short notice and based on a problem that may not exist by the time a solution started to be put in place.

Meanwhile, due to the complex process of liquifying natural gas, the overwhelming majority of LNG exports would be trapped in the Persian Gulf, resulting in slightly larger proportional blow to global gas supplies than to oil if the pipeline infrastructure is used to it’s full potential.

The reduction in the flow of LNG cargos would also impact fertilizer production in the rest of the world, acting as a double whammy on natural gas prices and the availability of fertilizer.

If the crisis persists, I will look into doing a long form article on the potential implications for fertilizer supplies and by extension the potential for food price inflation.

Spare Capacity?

Amidst the potential reduction of oil flows to market of over 7 million barrels per day, the question on a lot of minds is to what degree is there spare capacity from oil producers to deliver additional supply.

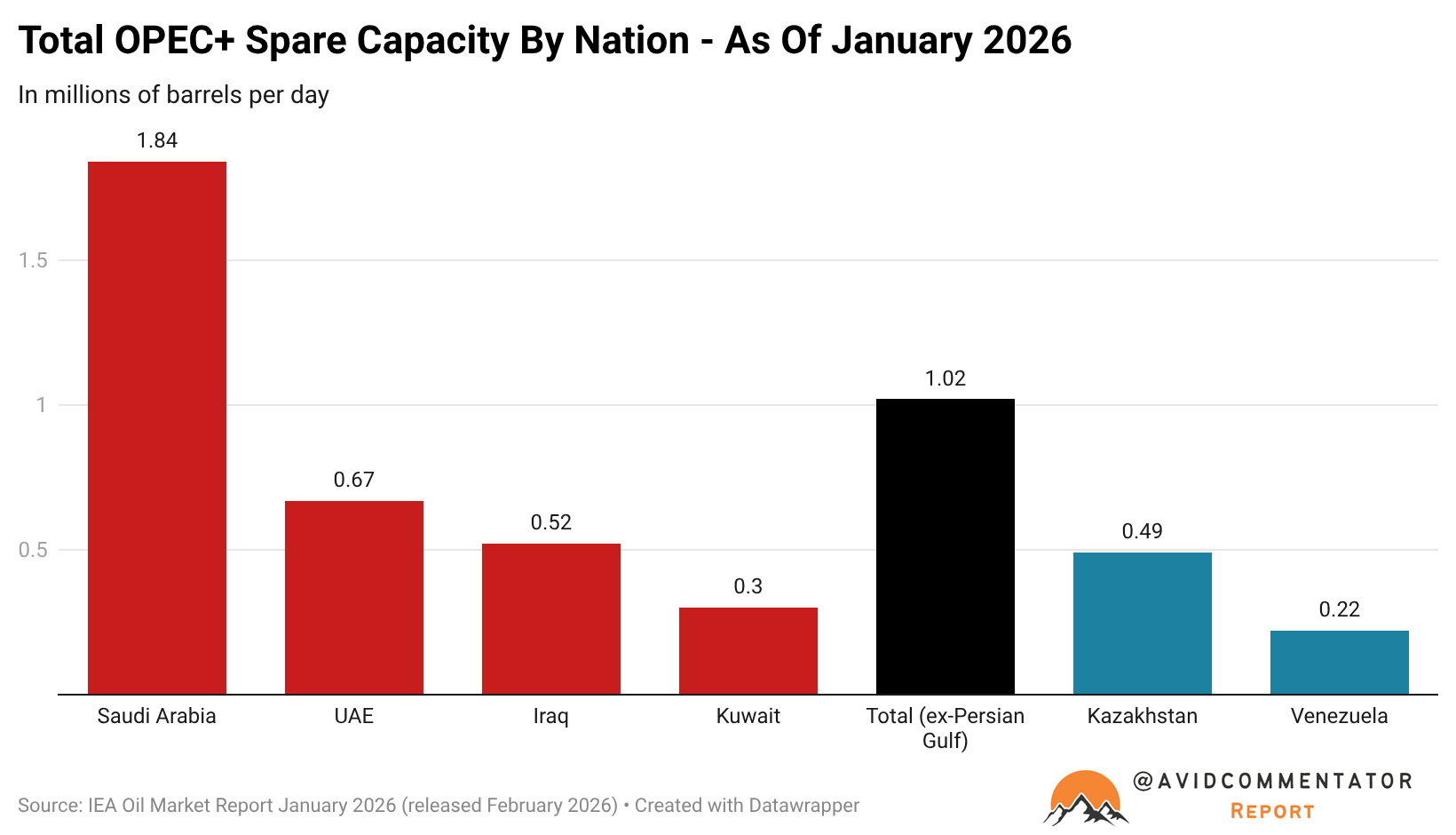

According to the January IEA Oil Market Report, total OPEC+ spare capacity is around 4.35 million barrels per day.

Which on paper is quite promising.

The problem is 76.5% of spare OPEC+ capacity is held by nations impacted by a potential closure of the Strait of Hormuz.

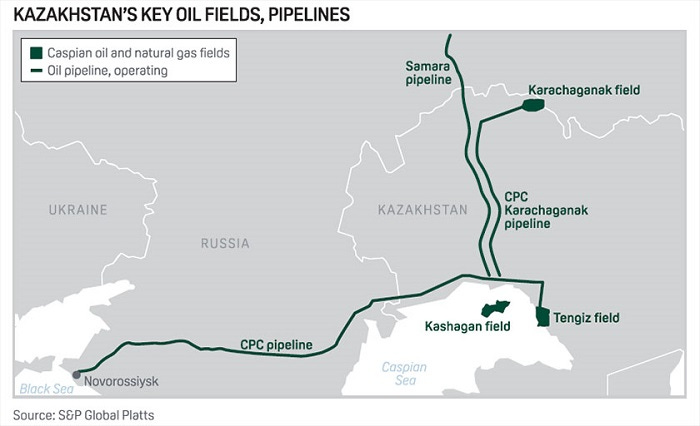

The largest unimpacted holder of spare capacity is Kazakhstan, with 490,000 barrels per day of extra capacity.

But this comes with potential issues of its own, due to the lack of access to open sea lanes, Kazakh oil flows through pipelines to Russian Black Sea ports for export.

The next greatest holder of spare capacity is Venezuela, with 220,000 barrels per day.

To what degree that capacity can be brought to market on a short term basis is an open question.

The Takeaway

If for whatever reason transits of commercial shipping through the Strait of Hormuz were blocked on a protracted basis, there is scope for around half of oil flows to be redirected on paper.

While part of the short fall could be made up by other nations outside the region ramping up production, the reality is that this would make a dent in the problem, but it wouldn’t solve it.

All in all, the world could be left short potentially over 5 million barrels a day of oil on a short term basis.

It’s also worth noting that from a purely financial perspective this would not be an awful scenario for the Saudi’s.

A large majority of their current production could still be exported and prices would be dramatically higher than they are now.

A protracted closure of the Strait of Hormuz represents a nightmare scenario, whether it be due to passage being directly impeded by attacks or the lack of insurance coverage on ships attempting to make the transit.

Ultimately, this is just one nightmare scenario of several currently potentially in play, after all it could be worse, we could be looking an Iranian attempt at the wholesale destruction of Gulf State oil infrastructure.

— If you would like to help support my work by making a one off donation that would be much appreciated, you can do so via Paypal here or via Buy me a coffee.

If you would like to support my work on an ongoing basis, you can do so by subscribing to my Substack or via Paypal here

Thank you for your readership.

A swarm of Shahed drones could easily take out the Saudi pipeline.

Pretty good. You could expand the article slightly by stating:

- we're going into a Northern Hemisphere summer so gas demand should be lower,

- Countries would start releasing from their strategic oil reserves,

- Some ships headed to China are passing through the straight.

Also:

- Iran's missile supply is in rapid decline,

- There drone production capability is in rapid decline.

I would guess that Iran can limit tanker flow for two weeks before they run out of weapons so the impact is going to be very short term.